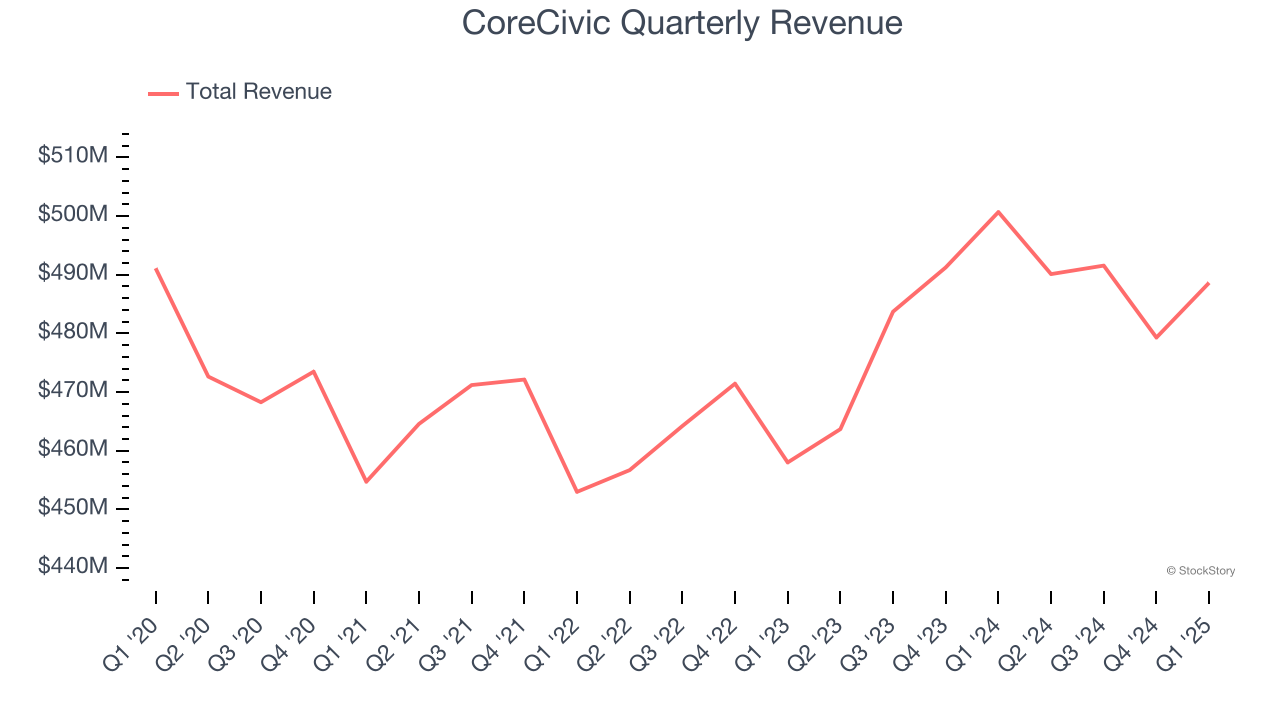

Private prison operator CoreCivic (NYSE: CXW) beat Wall Street’s revenue expectations in Q1 CY2025, but sales fell by 2.4% year on year to $488.6 million. Its non-GAAP profit of $0.23 per share was 79.7% above analysts’ consensus estimates.

Is now the time to buy CoreCivic? Find out by accessing our full research report, it’s free.

CoreCivic (CXW) Q1 CY2025 Highlights:

- Revenue: $488.6 million vs analyst estimates of $476.5 million (2.4% year-on-year decline, 2.5% beat)

- Adjusted EPS: $0.23 vs analyst estimates of $0.13 (79.7% beat)

- Adjusted EBITDA: $80.99 million vs analyst estimates of $70.87 million (16.6% margin, 14.3% beat)

- EBITDA guidance for the full year is $335 million at the midpoint, above analyst estimates of $324.5 million

- Market Capitalization: $2.52 billion

Damon T. Hininger, CoreCivic's Chief Executive Officer, commented, "2025 is off to a strong start for CoreCivic. First quarter occupancy in CoreCivic facilities reached 77.0% of available capacity, an increase from 75.2% in the first quarter of last year. Based on cost management and increased bed utilization, particularly from U.S. Immigration and Customs Enforcement (ICE), we exceeded our internal expectations for the first quarter. Additionally, we have begun to re-activate three previously idle facilities under multiple agreements with ICE. Based on the first quarter's results and activation activity, we are increasing our annual financial guidance.

Company Overview

Originally founded in 1983 as the first private prison company in the United States, CoreCivic (NYSE: CXW) operates correctional facilities, detention centers, and residential reentry programs for government agencies across the United States.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $1.95 billion in revenue over the past 12 months, CoreCivic is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, CoreCivic struggled to increase demand as its $1.95 billion of sales for the trailing 12 months was close to its revenue five years ago. This shows demand was soft, a poor baseline for our analysis.

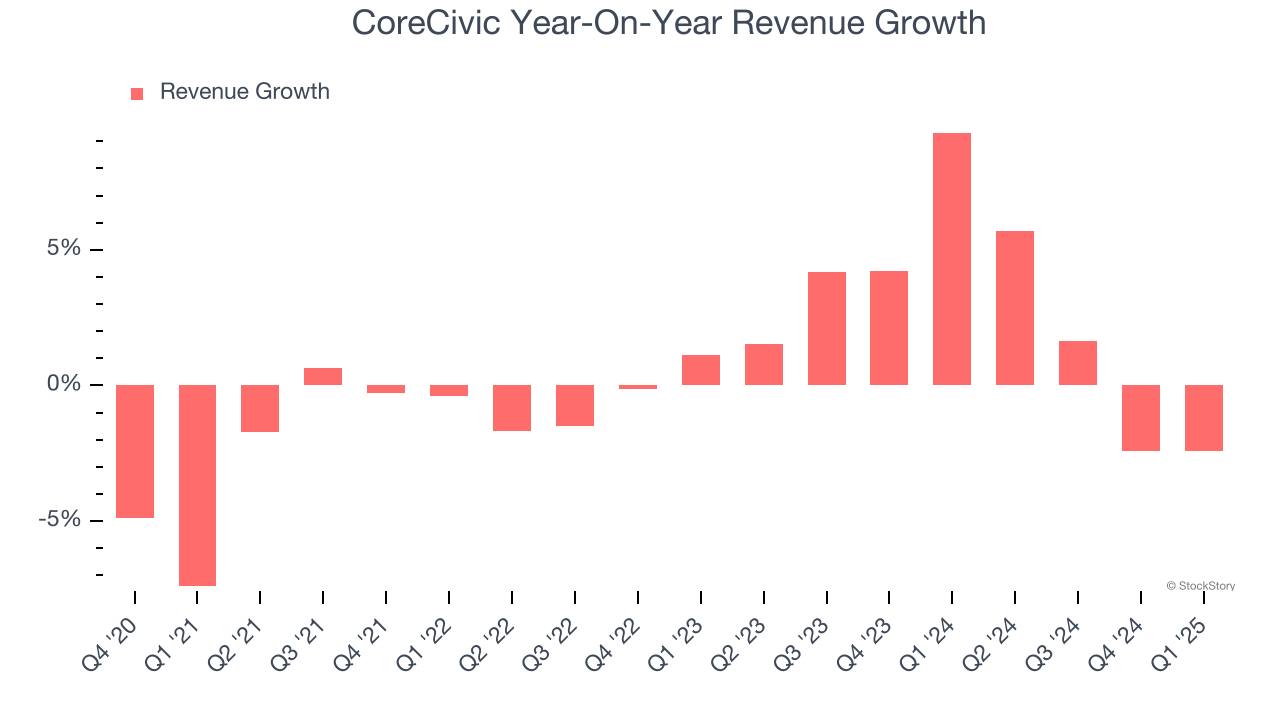

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. CoreCivic’s annualized revenue growth of 2.6% over the last two years is above its five-year trend, but we were still disappointed by the results.

This quarter, CoreCivic’s revenue fell by 2.4% year on year to $488.6 million but beat Wall Street’s estimates by 2.5%.

Looking ahead, sell-side analysts expect revenue to grow 11.7% over the next 12 months, an improvement versus the last two years. This projection is noteworthy and implies its newer products and services will catalyze better top-line performance.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

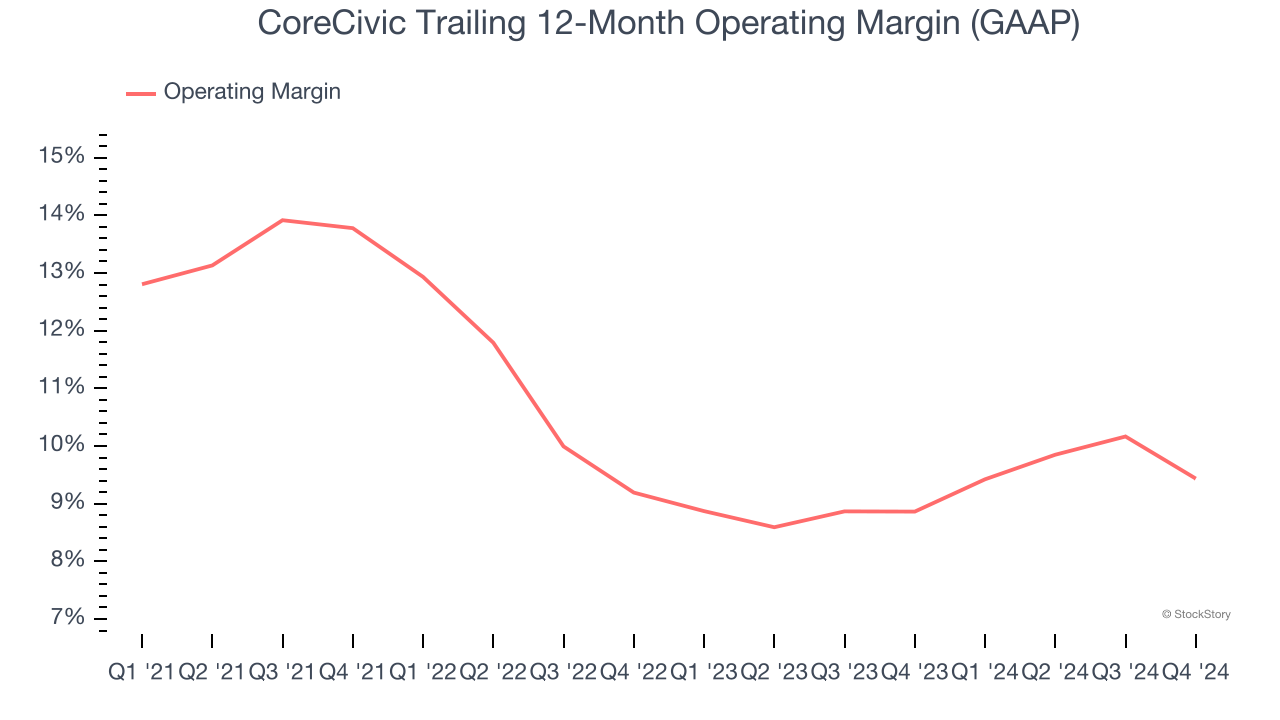

CoreCivic has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 10.7%, higher than the broader business services sector.

Looking at the trend in its profitability, CoreCivic’s operating margin decreased by 3.7 percentage points over the last five years. Even though its historical margin was healthy, shareholders will want to see CoreCivic become more profitable in the future.

in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

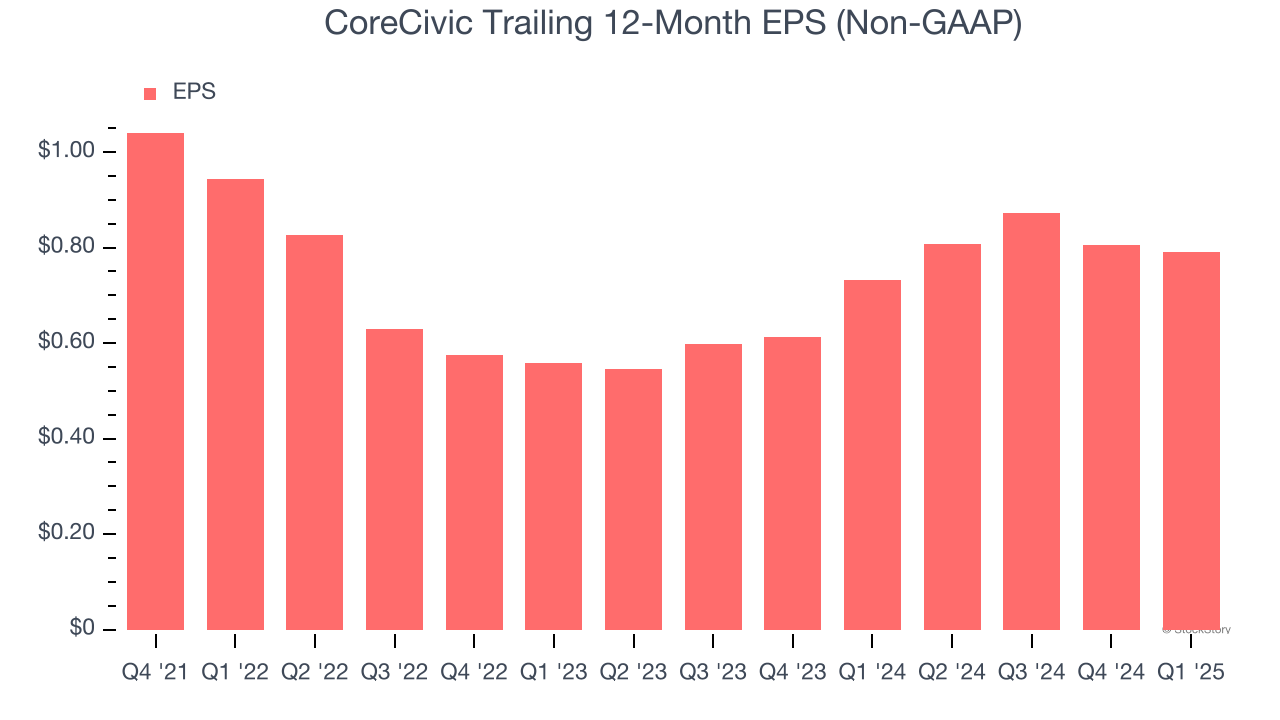

Revenue trends explain a company’s historical growth, but the change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

CoreCivic’s full-year EPS dropped 18.1%, or 5.7% annually, over the last three years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, CoreCivic’s low margin of safety could leave its stock price susceptible to large downswings.

In Q1, CoreCivic reported EPS at $0.23, down from $0.25 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects CoreCivic’s full-year EPS of $0.79 to grow 12.6%.

Key Takeaways from CoreCivic’s Q1 Results

We were impressed by how significantly CoreCivic blew past analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 3.2% to $23.35 immediately following the results.

CoreCivic had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.