Online advertising giant Alphabet (NASDAQ: GOOGL) reported Q2 CY2025 results beating Wall Street’s revenue expectations, with sales up 13.8% year on year to $96.43 billion. Its GAAP profit of $2.31 per share was 5.7% above analysts’ consensus estimates.

Is now the time to buy Alphabet? Find out by accessing our full research report, it’s free.

Alphabet (GOOGL) Q2 CY2025 Highlights:

- Revenue: $96.43 billion vs analyst estimates of $93.98 billion (2.6% beat)

- Operating Profit (GAAP): $31.27 billion vs analyst estimates of $31.09 billion (0.6% beat)

- EPS (GAAP): $2.31 vs analyst estimates of $2.19 (5.7% beat)

- Google Search Revenue: $0.02 vs analyst estimates of $52.92 billion (2.4% beat)

- Google Cloud Revenue: $0.04 vs analyst estimates of $13.12 billion (3.8% beat)

- YouTube Revenue: $9.80 billion vs analyst estimates of $9.58 billion (2.3% beat)

- Google Services Operating Profit: $0.01 vs analyst estimates of $32.77 billion (small beat)

- Google Cloud Operating Profit: $0.26 vs analyst estimates of $2.24 billion (26.2% beat)

- Operating Margin: 32.4%, in line with the same quarter last year

- "With this strong and growing demand for our Cloud products and services, we are increasing our investment in capital expenditures in 2025 to approximately $85 billion and are excited by the opportunity ahead" - CEO

- Free Cash Flow Margin: 5.5%, down from 15.9% in the same quarter last year

- Market Capitalization: $2.33 trillion

Sundar Pichai, CEO, said: "We had a standout quarter, with robust growth across the company. We are leading at the frontier of AI and shipping at an incredible pace. AI is positively impacting every part of the business, driving strong momentum. Search delivered double-digit revenue growth, and our new features, like AI Overviews and AI Mode, are performing well. We continue to see strong performance in YouTube as well as subscriptions offerings. And Cloud had strong growth in revenues, backlog and profitability. Its annual revenue run-rate is now more than $50 billion. With this strong and growing demand for our Cloud products and services, we are increasing our investment in capital expenditures in 2025 to approximately $85 billion and are excited by the opportunity ahead.”

Revenue Growth

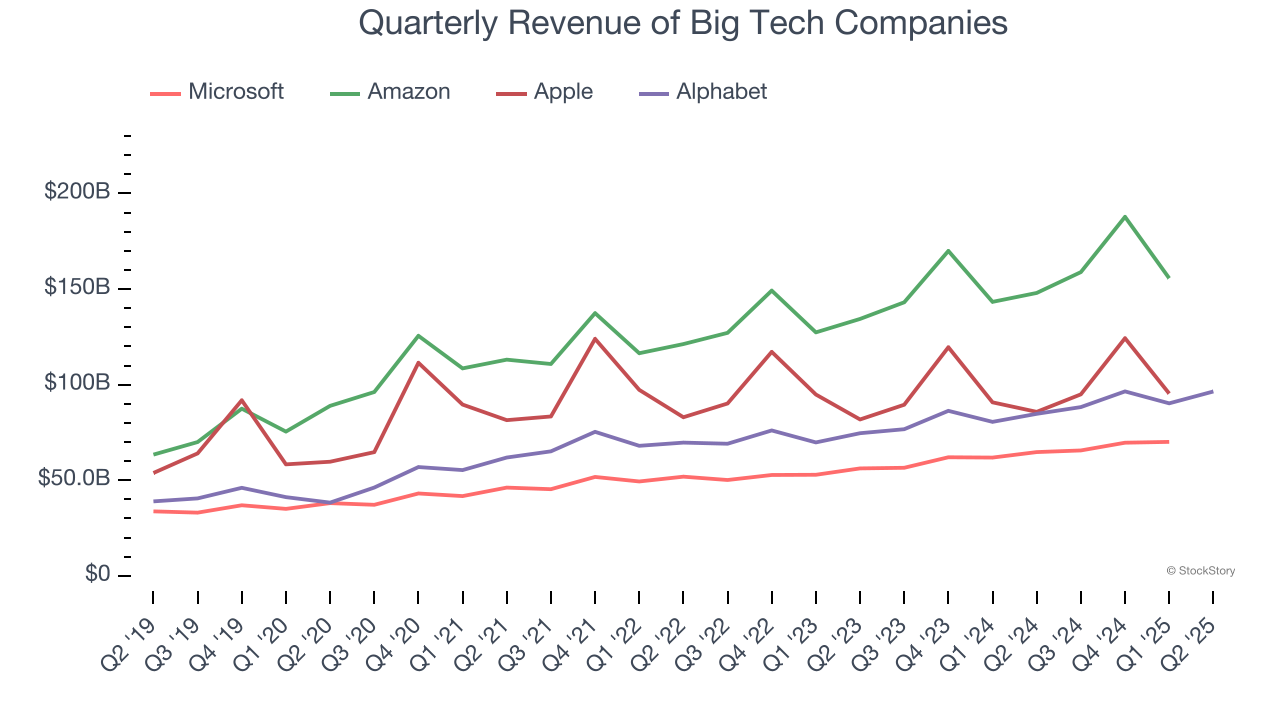

Alphabet shows that fast growth and massive scale can coexist despite conventional wisdom. The company’s revenue base of $166 billion five years ago has more than doubled to $371.4 billion in the last year, translating into an incredible 17.5% annualized growth rate.

Alphabet’s growth over the same period was also higher than its big tech peers, Amazon (16.6%), Microsoft (14.4%), and Apple (8%). Comparing the four is relevant because investors often pit them against each other to derive their valuations. With these benchmarks in mind, we think Alphabet is cheap.

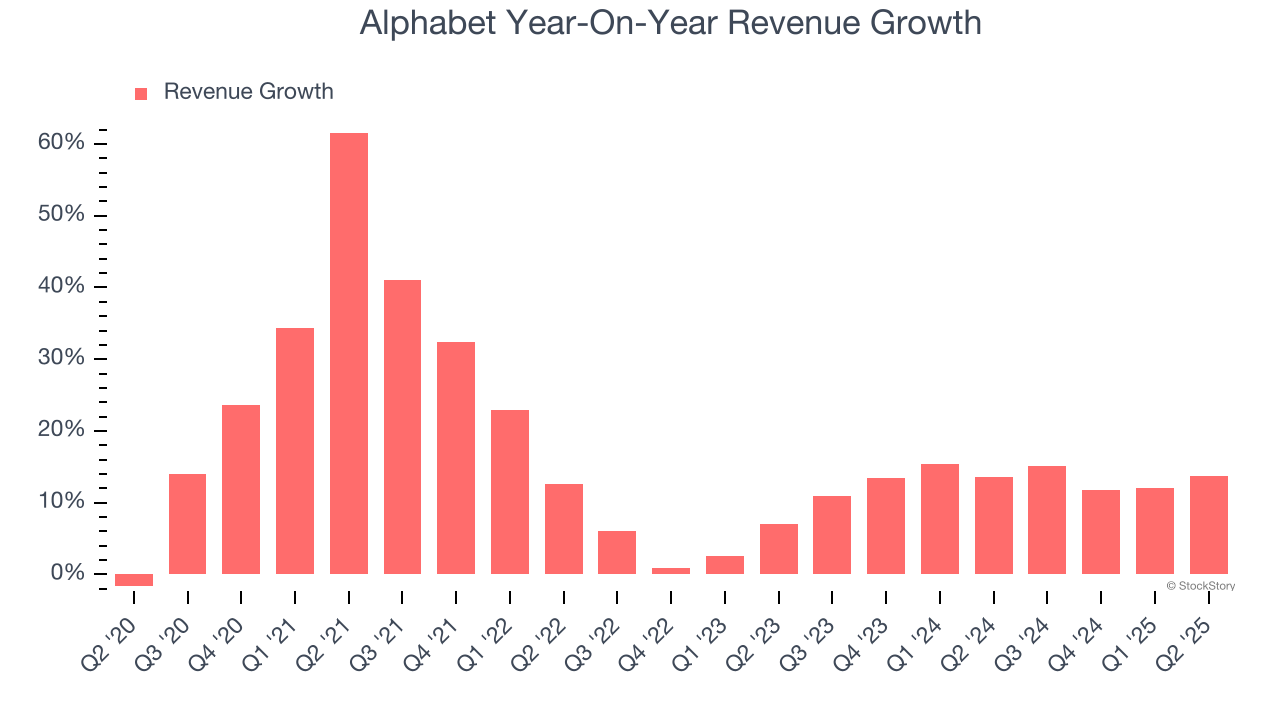

We at StockStory emphasize long-term growth, but for big tech companies, a half-decade historical view may miss emerging trends in AI. Alphabet’s annualized revenue growth of 13.3% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Alphabet reported year-on-year revenue growth of 13.8%, and its $96.43 billion of revenue exceeded Wall Street’s estimates by 2.6%. Looking ahead, sell-side This projection is still healthy and illustrates the market sees some success for its newer products.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Google Search: Alphabet’s Bread-and-Butter

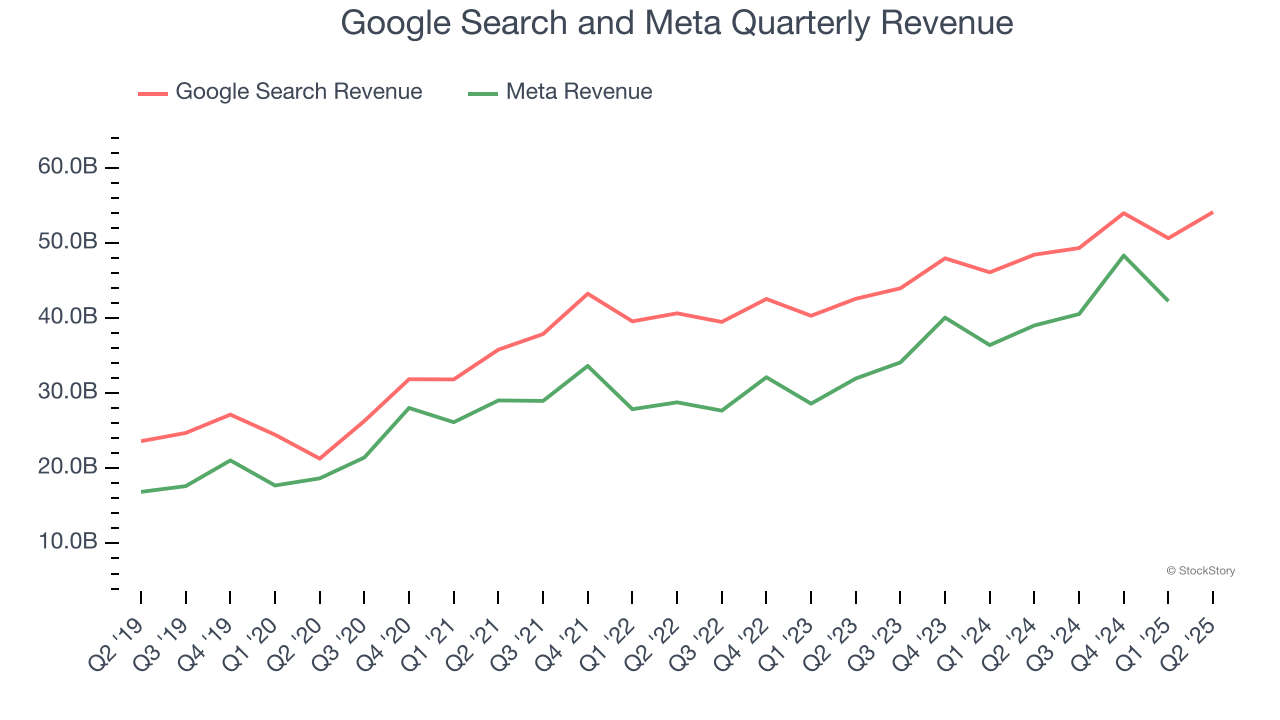

The most topical question surrounding Alphabet today is: “Will new Generative-AI products like ChatGPT and Meta AI disrupt Google Search and its 80%+ market share?”.

Although OpenAI (creator of ChatGPT) doesn’t disclose its financials, we can gain further insight by comparing Google Search to Meta and Microsoft’s Bing. Meta essentially has a monopoly in social media advertising and is creeping into search with Meta AI, which is powered by its Llama large language model, while Bing is the distant number two search engine that benefits from its integration with ChatGPT.

Starting with Alphabet, Google Search is by far the most considerable portion of its revenue at 56.1%, and it grew at a 16.3% annualized rate over the last five years, slower than total revenue. The previous two years also saw deceleration as it grew by 12.3% annually, though this isn’t concerning since it’s still expanding quickly.

On the other hand, its two-year result was lower than Meta’s 21.8%, showing digital advertising dollars could be flowing to Meta because of its improved AI algorithms and targeting capabilities. Alphabet bulls would argue this trend could reverse because the return on investment from keyword-driven advertising is more tangible, but that hasn’t been the case lately.

Quarterly performance is particularly relevant for Alphabet because it captures the growth of AI and signals whether investors are overestimating its competitive impact. Bulls can rejoice as Google Search revenue exceeded expectations in Q2, outperforming Wall Street Consensus by 2.4%. The segment recorded a hearty year-on-year increase of 11.7%.

While this was slower than Bing’s 23%, it’s important to consider that Bing has a much smaller revenue base and doesn’t pose a significant threat yet. Still, Alphabet must continue topping Wall Street’s Google Search projections and performing well in other segments like Google Cloud Platform and YouTube to win the debate.

Key Takeaways from Alphabet’s Q2 Results

It was encouraging to see Alphabet narrowly top analysts’ revenue expectations this quarter, as Google Cloud Platform, Google Search, and YouTube all beat. We were also glad its operating profit in the Services and Cloud segments outperformed Wall Street’s estimates. On the other hand, management stated that "we are increasing our investment in capital expenditures in 2025 to approximately $85 billion...." Overall, we think this was a solid quarter with some key areas of upside, but the market could be concerned about deteriorating cash generation due to higher capex forecasts, and shares traded down 1.3% to $187.88 immediately after reporting.

Is Alphabet an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.