While the S&P 500 is up 13.2% since November 2025, Zebra (currently trading at $246.68 per share) has lagged behind, posting a return of 8%. This might have investors contemplating their next move.

Is ZBRA a buy right now? Or is its underperformance reflective of its business quality?

Why Does ZBRA Stock Spark Debate?

Taking its name from the black and white stripes of barcodes, Zebra Technologies (NASDAQ: ZBRA) provides barcode scanners, mobile computers, RFID systems, and other data capture technologies that help businesses track assets and optimize operations.

Two Positive Attributes:

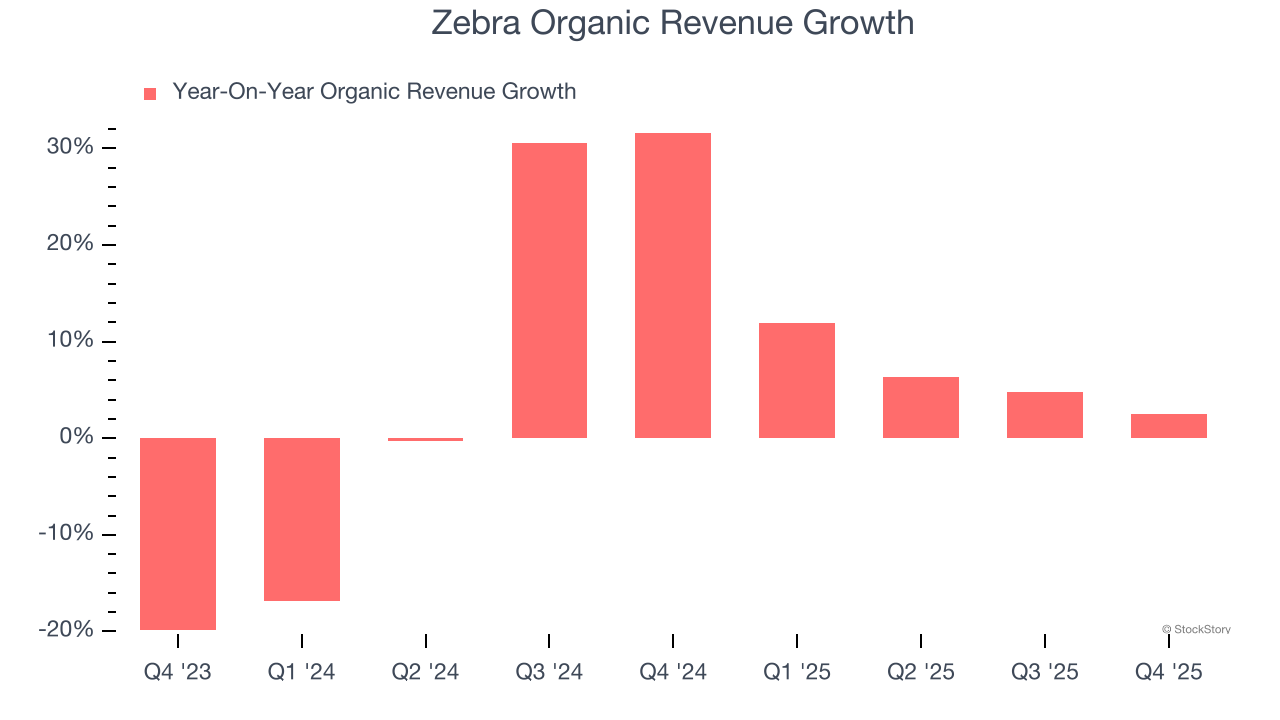

1. Core Business Firing on All Cylinders

In addition to reported revenue, organic revenue is a useful data point for analyzing Specialized Technology companies. This metric gives visibility into Zebra’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Zebra’s organic revenue averaged 12.5% year-on-year growth. This performance was impressive and shows it can expand quickly without relying on expensive (and risky) acquisitions.

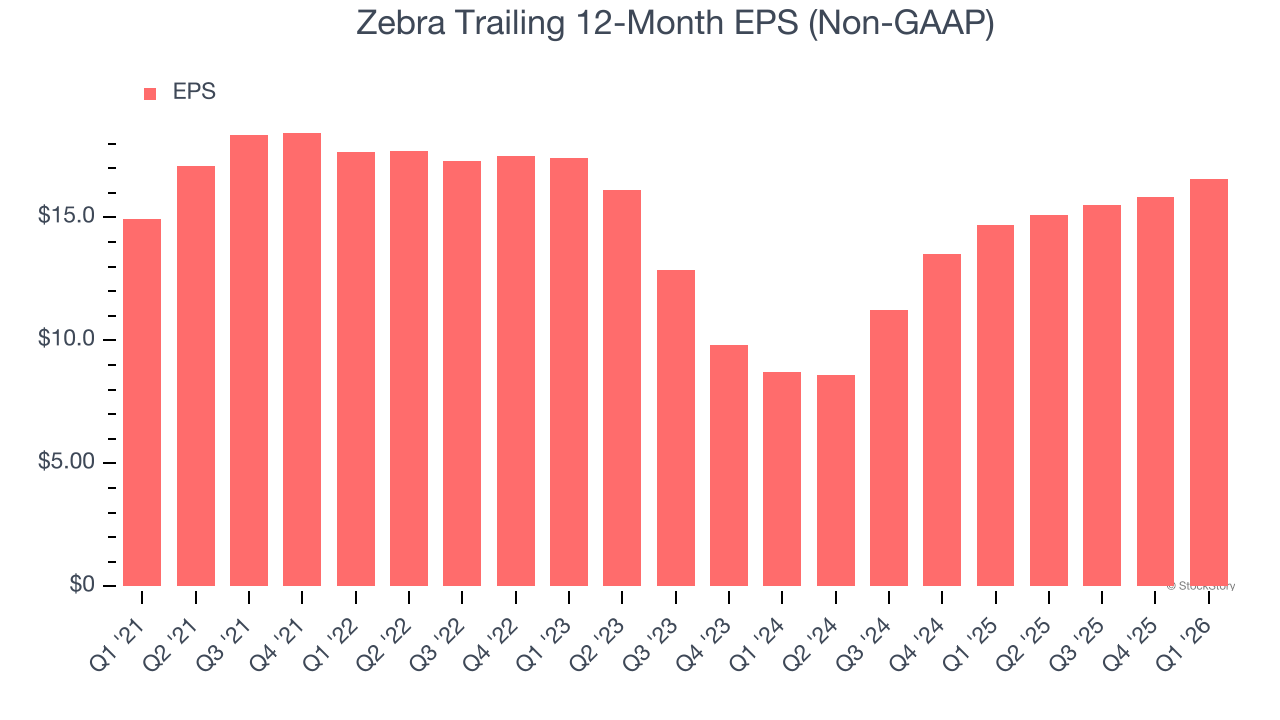

2. EPS Surges Higher Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Zebra’s EPS grew at an astounding 37.9% compounded annual growth rate over the last two years, higher than its 13.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

One Reason to be Careful:

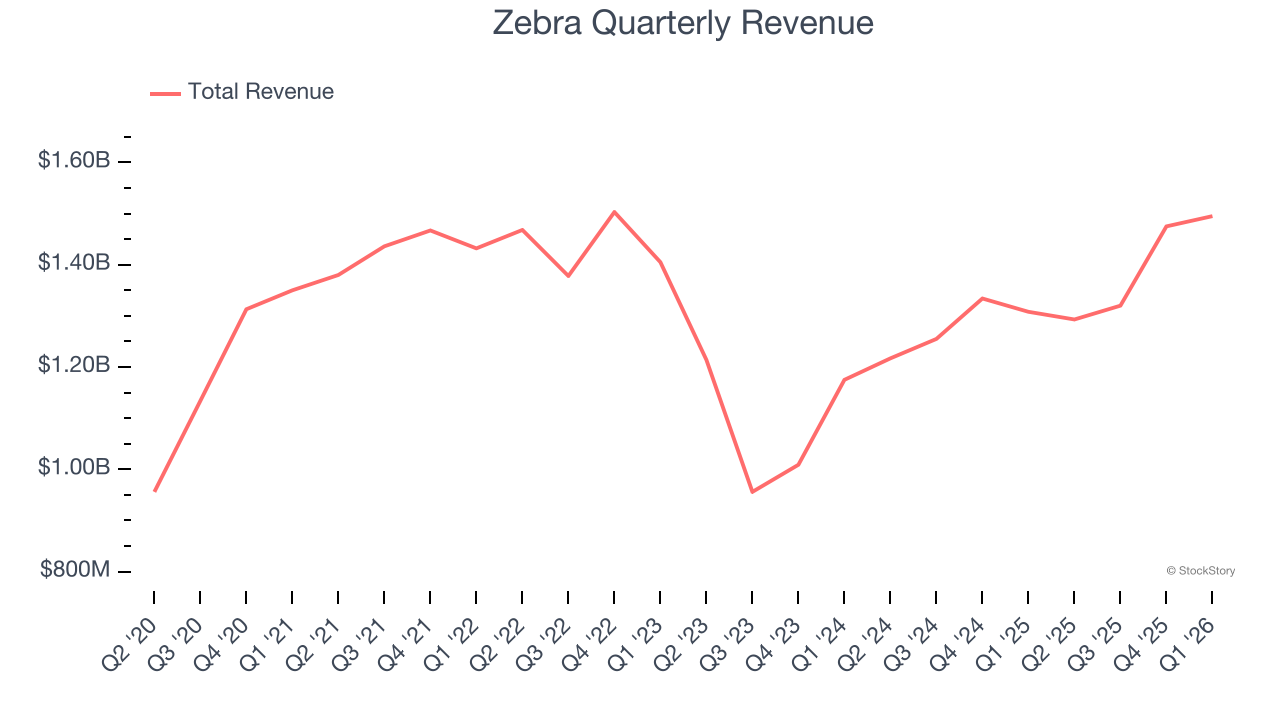

Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Zebra’s 3.3% annualized revenue growth over the last five years was tepid. This wasn’t a great result compared to the rest of the business services sector, but there are still things to like about Zebra.

Final Judgment

Zebra’s positive characteristics outweigh the negatives. With its shares lagging the market recently, the stock trades at 13.8× forward P/E (or $246.68 per share). Is now a good time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Zebra

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month - FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.