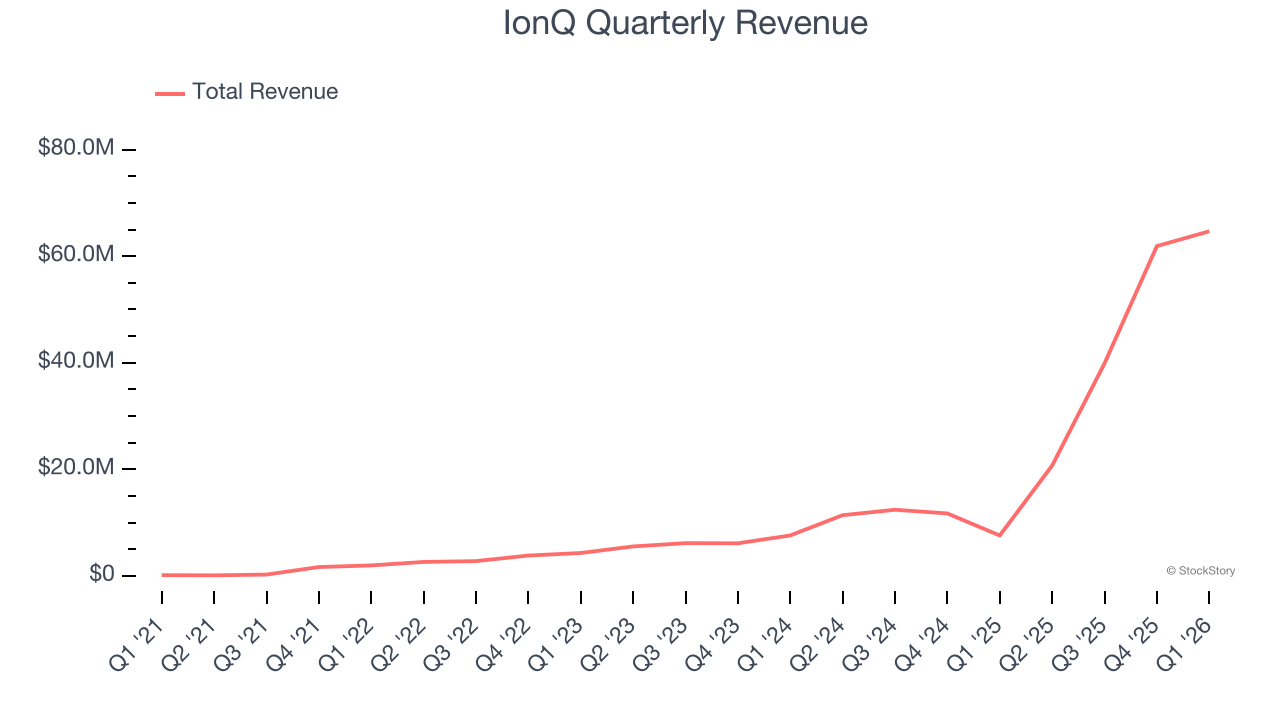

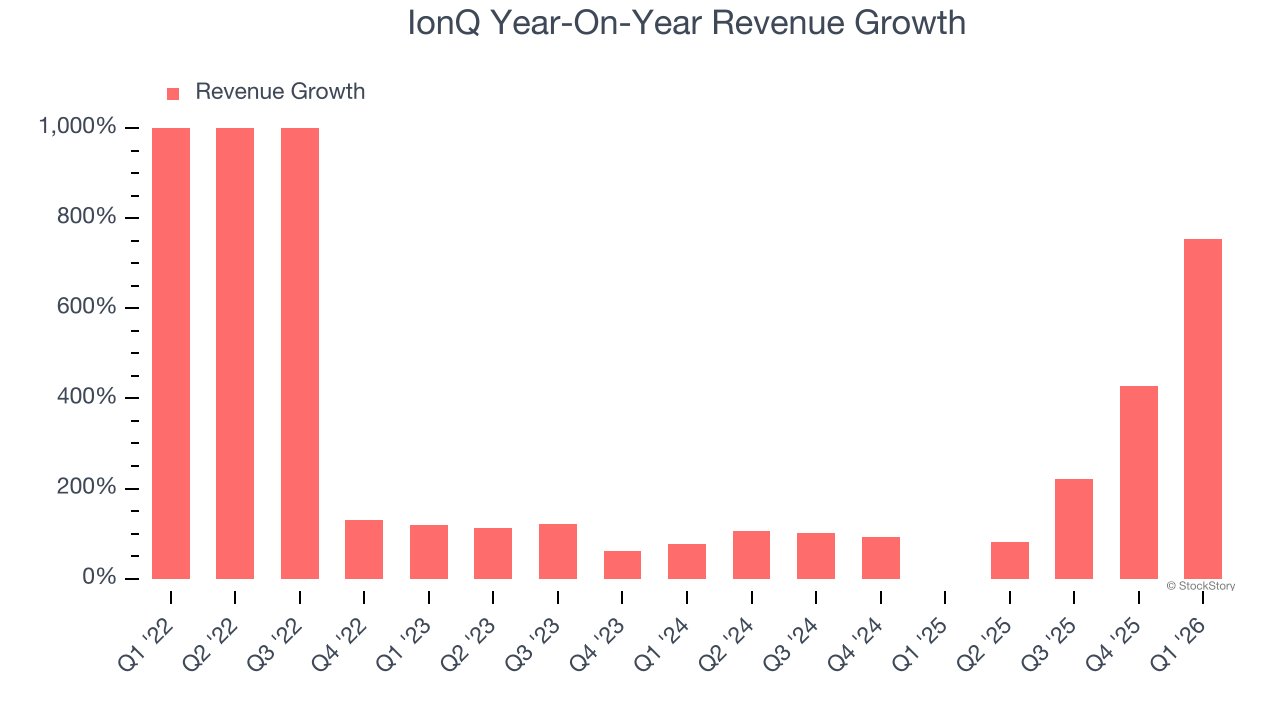

Quantum computing company IonQ (NYSE: IONQ) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 755% year on year to $64.67 million. On top of that, next quarter’s revenue guidance ($66.5 million at the midpoint) was surprisingly good and 22.1% above what analysts were expecting. Its non-GAAP loss of $0.34 per share was 37.5% below analysts’ consensus estimates.

Is now the time to buy IonQ? Find out by accessing our full research report, it’s free.

IonQ (IONQ) Q1 CY2026 Highlights:

- Revenue: $64.67 million vs analyst estimates of $49.73 million (755% year-on-year growth, 30% beat)

- Adjusted EPS: -$0.34 vs analyst expectations of -$0.25 (37.5% miss)

- Adjusted EBITDA: -$96.75 million (-150% margin, 170% year-on-year decline, large miss)

- The company lifted its revenue guidance for the full year to $265 million at the midpoint from $235 million, a 12.8% increase

- EBITDA guidance for the full year is -$320 million at the midpoint, above analyst estimates of -$321 million

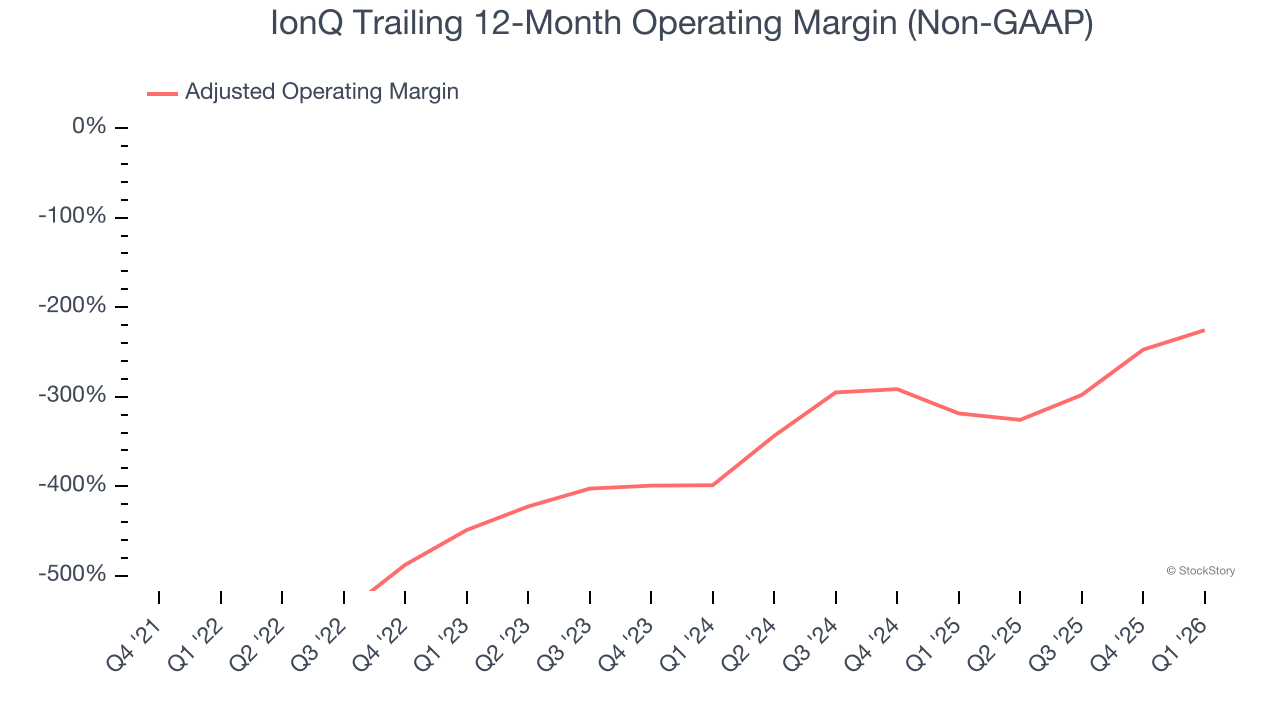

- Operating Margin: -420%, up from -1,000% in the same quarter last year

- Free Cash Flow was -$159.4 million compared to -$35.33 million in the same quarter last year

- Market Capitalization: $17.6 billion

Company Overview

Founded by quantum physics pioneers from the University of Maryland and Duke University in 2015, IonQ (NYSE: IONQ) develops quantum computers that process information using trapped ions to solve complex computational problems beyond the capabilities of traditional computers.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $187.1 million in revenue over the past 12 months, IonQ is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

As you can see below, IonQ grew its sales at an incredible 163% compounded annual growth rate over the last four years. This is an encouraging starting point for our analysis because it shows IonQ’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a stretched historical view may miss recent innovations or disruptive industry trends. IonQ’s annualized revenue growth of 172% over the last two years is above its four-year trend, suggesting its demand was strong and recently accelerated.

This quarter, IonQ reported magnificent year-on-year revenue growth of 755%, and its $64.67 million of revenue beat Wall Street’s estimates by 30%. Company management is currently guiding for a 221% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 38.4% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is noteworthy and indicates the market is baking in success for its products and services.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Adjusted Operating Margin

IonQ’s high expenses have contributed to an average adjusted operating margin of negative 278% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, IonQ’s adjusted operating margin rose over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

In Q1, IonQ generated a negative 221% adjusted operating margin.

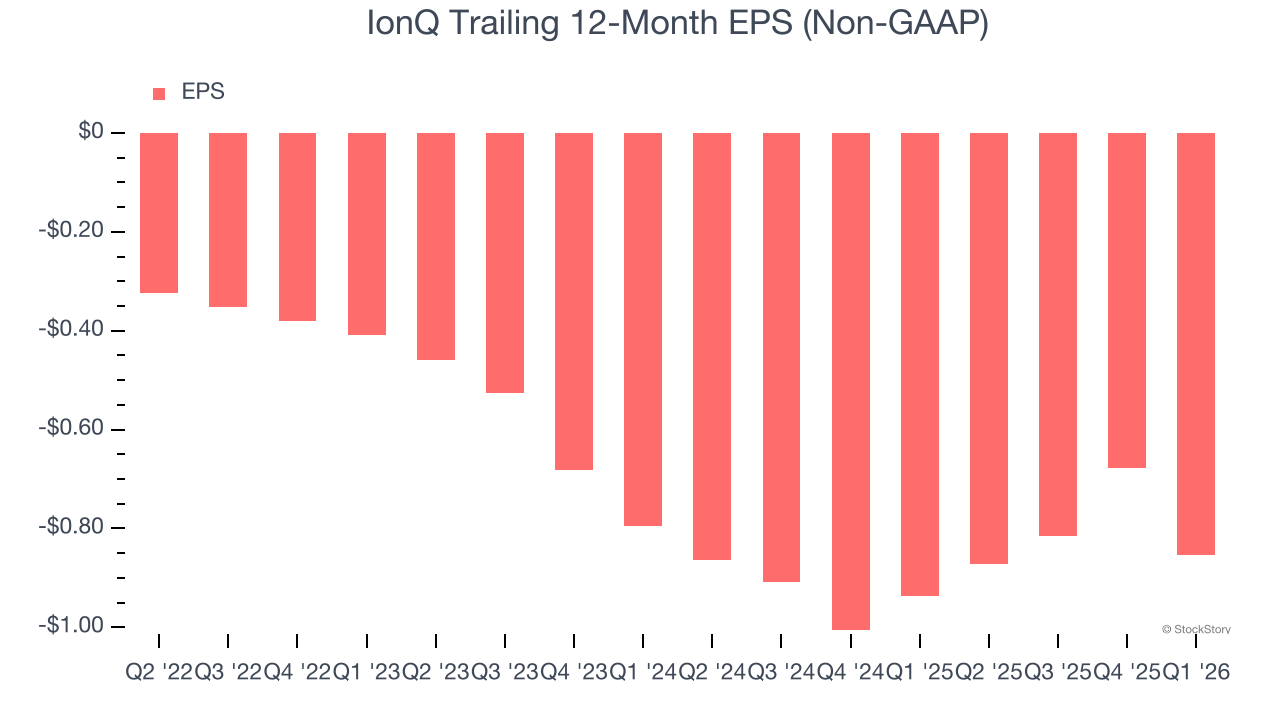

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

IonQ’s earnings losses deepened over the last four years as its EPS dropped 32.1% annually. We’ll keep a close eye on the company as diminishing earnings could imply changing secular trends and preferences.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For IonQ, its two-year annual EPS declines of 3.6% show it’s still underperforming. These results were bad no matter how you slice the data, but given it was successful in other measures of financial health, we’re hopeful IonQ can generate earnings growth in the future.

In Q1, IonQ reported adjusted EPS of negative $0.34, down from negative $0.16 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects IonQ to perform poorly. Analysts forecast its full-year EPS of negative $0.85 will tumble to negative $0.99.

Key Takeaways from IonQ’s Q1 Results

We were impressed by how significantly IonQ blew past analysts’ revenue expectations this quarter. We were also glad its revenue guidance for next quarter trumped Wall Street’s estimates. On the other hand, its EBITDA missed badly, and its EPS missed as well. Overall, we think this was a mixed quarter. Investors were likely hoping for more, and shares traded down 5.4% to $49.86 immediately after reporting.

So do we think IonQ is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).