Dell (DELL) stock has pulled back sharply despite robust demand for its artificial intelligence (AI)-optimized servers. Shares are down about 20% over the past three months and have fallen roughly 26% from their 52-week high of $168.08. This decline is largely driven by concerns about profitability rather than revenue growth.

The primary issue weighing on Dell stock has been margin pressure. As Dell continues to shift its product mix toward AI-optimized servers, margins have come under strain. These systems are seeing strong demand, but they are hurting margins. Moreover, a highly competitive environment is weighing on pricing, taking a toll on the company's overall margins. At the same time, inflation in component costs has pushed input expenses higher, further squeezing profitability.

The impact of these forces has been evident in Dell’s recent financial results. In the third quarter of fiscal 2026, Dell’s adjusted gross margin dropped 140 basis points to 21.1%. Over the first nine months of the fiscal year, adjusted gross margin was down an even steeper 190 basis points. Unsurprisingly, this margin compression dampened investor sentiment and contributed to the stock’s selloff.

Encouragingly, there are signs that the pressure on its margins may be easing. In the third quarter, Dell’s Infrastructure Solutions Group (ISG) showed meaningful sequential improvement. Its operating income rate rose by 360 basis points to 12.4% of revenue, supported by a healthier mix of AI products, improving margins on AI servers, and stronger performance in storage solutions. This suggests Dell is beginning to scale its AI business more efficiently.

That operational progress flowed through to the bottom line. Its adjusted earnings came in at $2.59 per share, comfortably ahead of analysts’ expectations. Improved operating income and efficient cost management helped offset lingering margin challenges.

Is DELL Stock a Buy?

Dell is likely to benefit from strong demand for AI-focused servers and a growing and more diversified customer base. Moreover, an improvement in profitability could give Dell stock a significant boost.

During the third quarter, Dell booked $12.3 billion in AI server orders, lifting year-to-date (YTD) orders to $30 billion. Moreover, Dell is broadening its customer base, which augurs well for margin growth. Dell is no longer relying primarily on large customers. Orders are now coming from second-tier cloud service providers, neocloud operators, and sovereign customers, reflecting broader, more resilient demand and supporting longer-term growth.

Strong demand is translating into higher shipments. At the same time, Dell’s backlog climbed to $18.4 billion, providing strong visibility into future revenue.

Dell is seeing a recovery in traditional server demand. The quarter-over-quarter improvement in North America and EMEA points to increased IT modernization spending, especially on high-performance configurations.

Storage has been a comparatively softer area, with revenue slipping modestly year-over-year (YoY). However, Dell’s IP portfolio continues to attract demand, and its all-flash array portfolio has now posted two consecutive quarters of double-digit growth. These products are becoming more strategically valuable to the overall business as they carry higher margins.

Overall, Dell is well-positioned for continued growth in the coming quarters. Competitive pressures and higher input costs remain challenges, but they are likely to be offset by a healthier product mix, improving margins on AI servers, and momentum in storage. These factors could support an improvement in operating income over time.

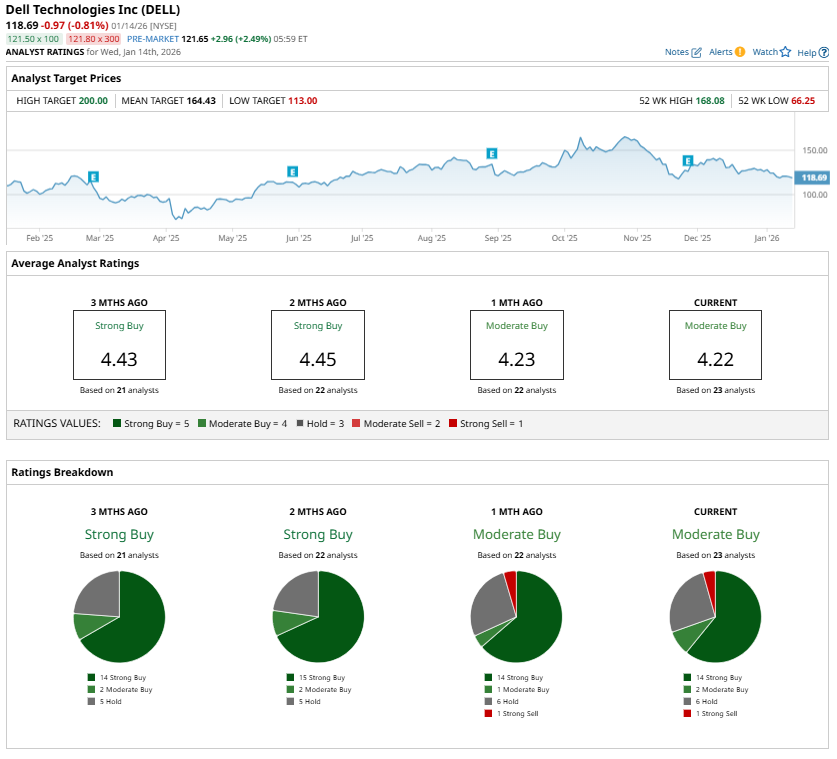

What Do Analysts Say?

Wall Street remains relatively cautious, maintaining a “Moderate Buy” consensus due to competition and margin headwinds. However, AI-driven opportunities, record order levels, a swelling backlog, an expanding global customer base, and signs of profit growth all point to sustained momentum.

Valuation further strengthens the investment case. Dell trades at 13.5 times forward earnings, which appears modest given analysts’ expectations for more than 15% earnings growth in fiscal 2027. For investors seeking exposure to AI infrastructure at an attractive valuation, DELL stock looks compelling near current levels.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Unusual Options Activity: 3 Multi-Leg Trades to Watch — SHOP, SBUX, and PINS

- Don’t Trade the Venezuela Headlines. Why We’re Skipping Oil Majors to Zero In on These Energy Stocks Instead.

- The Next Big AI Stock Winners Hiding in Plain Sight

- Why the S&P 500’s No. 1 Performer Is Invisible in Your Tech ETFs