Otis has been treading water for the past six months, recording a small return of 4.2% while holding steady at $97.90.

Is there a buying opportunity in Otis, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

We don't have much confidence in Otis. Here are three reasons why we avoid OTIS and a stock we'd rather own.

Why Is Otis Not Exciting?

Credited with inventing the first hydraulic passenger elevator, Otis Worldwide (NYSE: OTIS) is an elevator and escalator manufacturing, installation and service company.

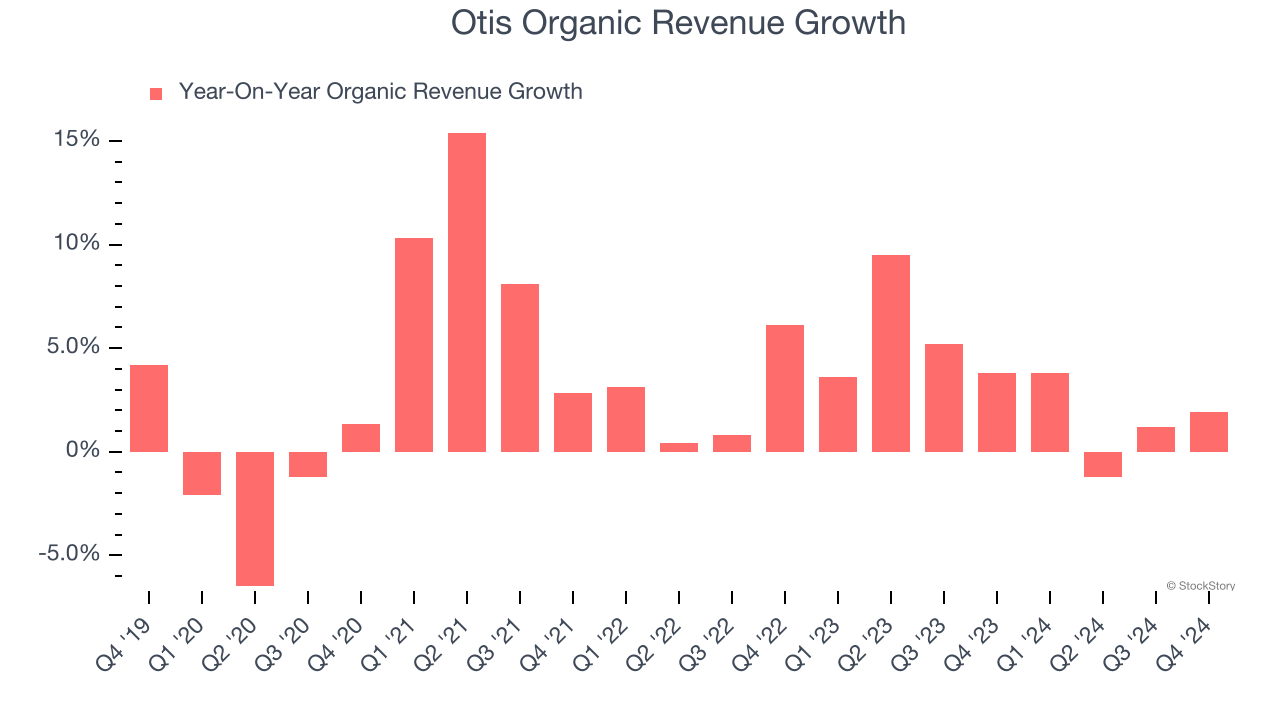

1. Slow Organic Growth Suggests Waning Demand In Core Business

In addition to reported revenue, organic revenue is a useful data point for analyzing General Industrial Machinery companies. This metric gives visibility into Otis’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Otis’s organic revenue averaged 3.5% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Otis’s revenue to stall, a slight deceleration versus its 2.5% annualized growth for the past two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

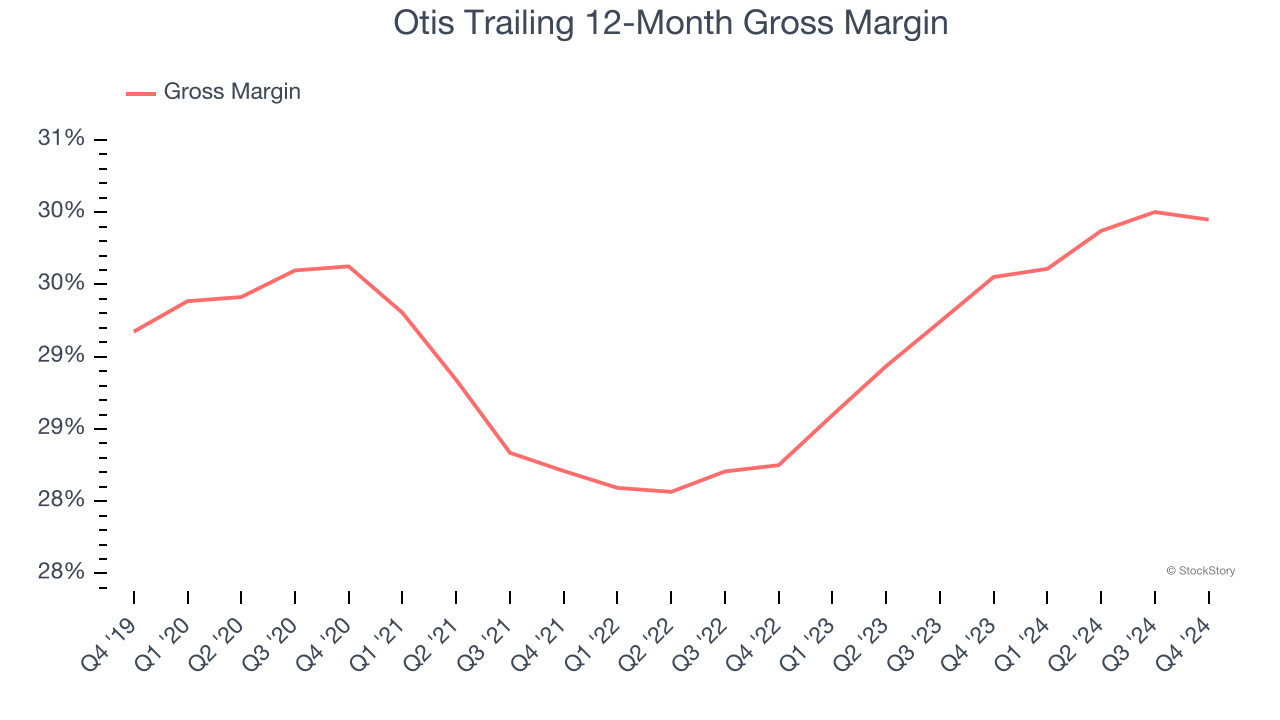

3. Low Gross Margin Hinders Flexibility

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

Otis’s gross margin is slightly below the average industrials company, giving it less room to invest in areas such as research and development. As you can see below, it averaged a 29.1% gross margin over the last five years. Said differently, Otis had to pay a chunky $70.88 to its suppliers for every $100 in revenue.

Final Judgment

Otis’s business quality ultimately falls short of our standards. That said, the stock currently trades at 24.6× forward price-to-earnings (or $97.90 per share). At this valuation, there’s a lot of good news priced in - you can find better investment opportunities elsewhere. We’d recommend looking at our favorite semiconductor picks and shovels play.

Stocks We Like More Than Otis

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.