Wrapping up Q4 earnings, we look at the numbers and key takeaways for the footwear stocks, including Wolverine Worldwide (NYSE: WWW) and its peers.

Before the advent of the internet, styles changed, but consumers mainly bought shoes by visiting local brick-and-mortar shoe, department, and specialty stores. Today, not only do styles change more frequently as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some footwear companies have made concerted efforts to adapt while those who are slower to move may fall behind.

The 8 footwear stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 2% while next quarter’s revenue guidance was in line.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 32.5% since the latest earnings results.

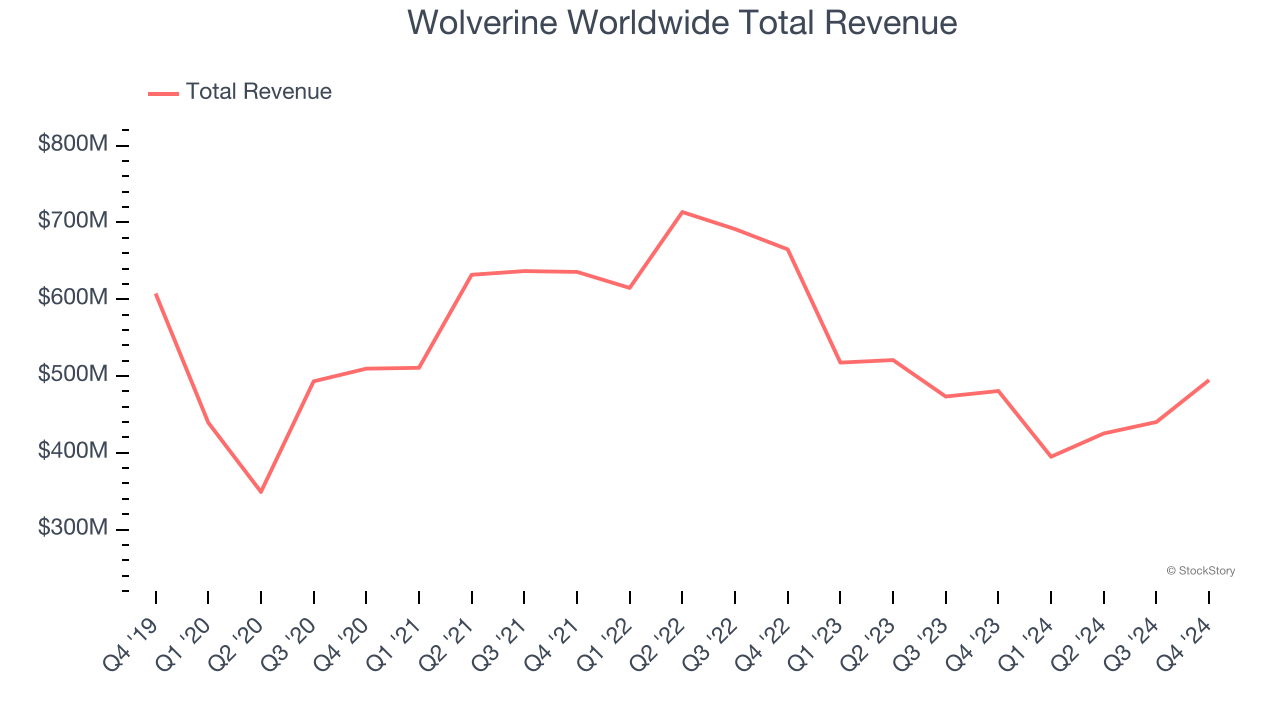

Wolverine Worldwide (NYSE: WWW)

Founded in 1883, Wolverine Worldwide (NYSE: WWW) is a global footwear company with a diverse portfolio of brands including Merrell, Hush Puppies, and Saucony.

Wolverine Worldwide reported revenues of $494.7 million, up 3% year on year. This print exceeded analysts’ expectations by 5.9%. Despite the top-line beat, it was still a slower quarter for the company with full-year EPS guidance missing analysts’ expectations.

“A year ago, we outlined an ambitious turnaround strategy composed of three chapters: stabilization, transformation, and inflection. We shared a plan to meaningfully strengthen the Company's balance sheet, expand profitability, and sequentially improve revenue trends – culminating with an inflection to growth in the final quarter of 2024,” said Chris Hufnagel, President and Chief Executive Officer of Wolverine Worldwide.

Wolverine Worldwide scored the biggest analyst estimates beat but had the weakest full-year guidance update of the whole group. Still, the market seems discontent with the results. The stock is down 24.7% since reporting and currently trades at $10.61.

Read our full report on Wolverine Worldwide here, it’s free.

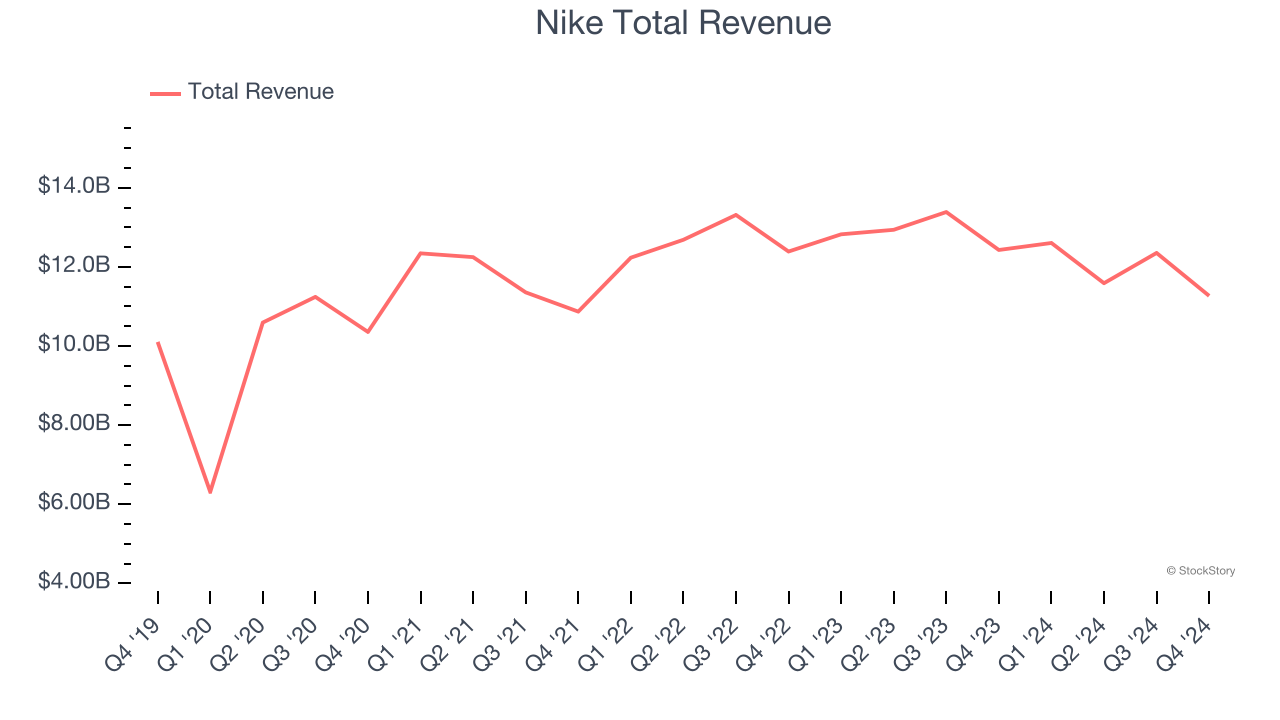

Best Q4: Nike (NYSE: NKE)

Originally selling Japanese Onitsuka Tiger sneakers as Blue Ribbon Sports, Nike (NYSE: NKE) is a global titan in athletic footwear, apparel, equipment, and accessories.

Nike reported revenues of $11.27 billion, down 9.3% year on year, outperforming analysts’ expectations by 2.3%. The business had a stunning quarter with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

The stock is down 24.7% since reporting. It currently trades at $54.09.

Is now the time to buy Nike? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Genesco (NYSE: GCO)

Spanning a broad range of styles, brands, and prices, Genesco (NYSE: GCO) sells footwear, apparel, and accessories through multiple brands and banners.

Genesco reported revenues of $745.9 million, flat year on year, falling short of analysts’ expectations by 5%. It was a softer quarter as it posted adjusted operating income in line with analysts’ estimates.

Genesco delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 44.8% since the results and currently trades at $17.93.

Read our full analysis of Genesco’s results here.

Deckers (NYSE: DECK)

Established in 1973, Deckers (NYSE: DECK) is a footwear and apparel conglomerate with a portfolio of lifestyle and performance brands.

Deckers reported revenues of $1.83 billion, up 17.1% year on year. This number topped analysts’ expectations by 5.5%. It was a strong quarter as it also produced a solid beat of analysts’ constant currency revenue estimates and an impressive beat of analysts’ EPS estimates.

Deckers achieved the fastest revenue growth and highest full-year guidance raise among its peers. The stock is down 53.3% since reporting and currently trades at $104.07.

Read our full, actionable report on Deckers here, it’s free.

Skechers (NYSE: SKX)

Synonymous with "dad shoe", Skechers (NYSE: SKX) is a footwear company renowned for its comfortable, stylish, and affordable shoes for all ages.

Skechers reported revenues of $2.21 billion, up 12.8% year on year. This result was in line with analysts’ expectations. Zooming out, it was a softer quarter as it logged a significant miss of analysts’ EPS estimates.

The stock is down 37.7% since reporting and currently trades at $47.18.

Read our full, actionable report on Skechers here, it’s free.

Market Update

As a result of the Fed’s rate hikes in 2022 and 2023, inflation has come down from frothy levels post-pandemic. The general rise in the price of goods and services is trending towards the Fed’s 2% goal as of late, which is good news. The higher rates that fought inflation also didn't slow economic activity enough to catalyze a recession. So far, soft landing. This, combined with recent rate cuts (half a percent in September 2024 and a quarter percent in November 2024) have led to strong stock market performance in 2024. The icing on the cake for 2024 returns was Donald Trump’s victory in the U.S. Presidential Election in early November, sending major indices to all-time highs in the week following the election. Still, debates around the health of the economy and the impact of potential tariffs and corporate tax cuts remain, leaving much uncertainty around 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.