The end of an earnings season can be a great time to discover new stocks and assess how companies are handling the current business environment. Let’s take a look at how Boeing (NYSE: BA) and the rest of the aerospace stocks fared in Q3.

Aerospace companies often possess technical expertise and have made significant capital investments to produce complex products. It is an industry where innovation is important, and lately, emissions and automation are in focus, so companies that boast advances in these areas can take market share. On the other hand, demand for aerospace products can ebb and flow with economic cycles and geopolitical tensions, which can be particularly painful for companies with high fixed costs.

The 15 aerospace stocks we track reported a mixed Q3. As a group, revenues missed analysts’ consensus estimates by 1.8% while next quarter’s revenue guidance was in line.

Luckily, aerospace stocks have performed well with share prices up 21.4% on average since the latest earnings results.

Boeing (NYSE: BA)

One of the companies that forms a duopoly in the commercial aircraft market, Boeing (NYSE: BA) develops, manufactures, and services commercial airplanes, defense products, and space systems.

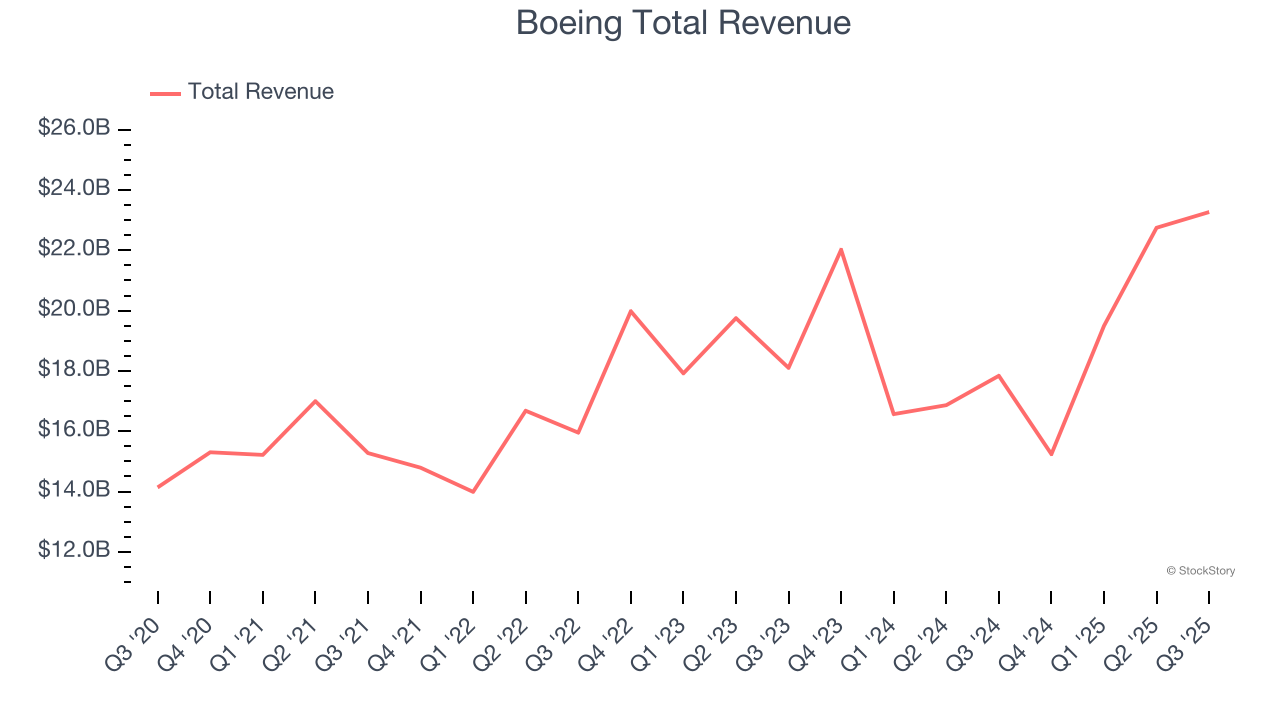

Boeing reported revenues of $23.27 billion, up 30.4% year on year. This print exceeded analysts’ expectations by 6.3%. Despite the top-line beat, it was still a softer quarter for the company with a significant miss of analysts’ adjusted operating income estimates and a significant miss of analysts’ EBITDA estimates.

"With a sustained focus on safety and quality, we achieved important milestones in our recovery as we generated positive free cash flow in the quarter and jointly agreed with the FAA in October to increase 737 production to 42 per month," said Kelly Ortberg, Boeing president and chief executive officer.

Boeing achieved the biggest analyst estimates beat of the whole group. Unsurprisingly, the stock is up 5% since reporting and currently trades at $234.36.

Read our full report on Boeing here, it’s free.

Best Q3: AAR (NYSE: AIR)

The first third-party MRO approved by the FAA for Safety Management System Requirements, AAR (NYSE: AIR) is a provider of aircraft maintenance services

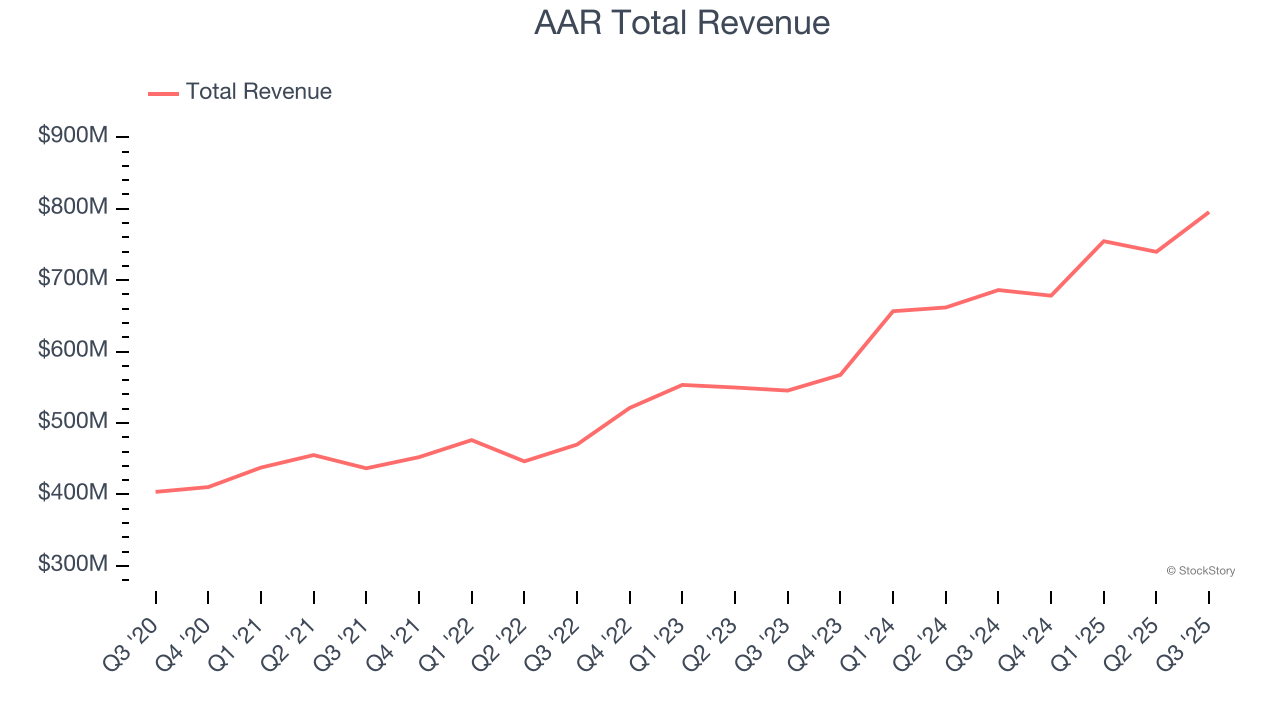

AAR reported revenues of $795.3 million, up 15.9% year on year, outperforming analysts’ expectations by 4.4%. The business had an exceptional quarter with an impressive beat of analysts’ adjusted operating income estimates and a solid beat of analysts’ revenue estimates.

The market seems happy with the results as the stock is up 7.7% since reporting. It currently trades at $97.

Is now the time to buy AAR? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: AerSale (NASDAQ: ASLE)

Providing a one-stop shop that integrates multiple services and product offerings, AerSale (NASDAQ: ASLE) delivers full-service support to mid-life commercial aircraft.

AerSale reported revenues of $71.19 million, down 13.9% year on year, falling short of analysts’ expectations by 30.5%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue estimates and a significant miss of analysts’ adjusted operating income estimates.

AerSale delivered the weakest performance against analyst estimates and slowest revenue growth in the group. Interestingly, the stock is up 9.6% since the results and currently trades at $7.66.

Read our full analysis of AerSale’s results here.

Curtiss-Wright (NYSE: CW)

Formed from a merger of 12 companies, Curtiss-Wright (NYSE: CW) provides a range of products and services to the aerospace, industrial, electronic, and maritime industries.

Curtiss-Wright reported revenues of $869.2 million, up 8.8% year on year. This print lagged analysts' expectations by 0.5%. Taking a step back, it was a satisfactory quarter as it also logged a solid beat of analysts’ adjusted operating income estimates but a slight miss of analysts’ revenue estimates.

The stock is up 3.5% since reporting and currently trades at $605.50.

Read our full, actionable report on Curtiss-Wright here, it’s free.

Textron (NYSE: TXT)

Listed on the NYSE in 1947, Textron (NYSE: TXT) provides products and services in the aerospace, defense, industrial, and finance sectors.

Textron reported revenues of $3.60 billion, up 5.1% year on year. This number missed analysts’ expectations by 1.9%. Zooming out, it was a mixed quarter as it also recorded a solid beat of analysts’ EBITDA estimates but a miss of analysts’ revenue estimates.

The stock is up 13.6% since reporting and currently trades at $93.80.

Read our full, actionable report on Textron here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.