Tutor Perini currently trades at $84.22 and has been a dream stock for shareholders. It’s returned 419% since April 2021, blowing past the S&P 500’s 70.2% gain. The company has also beaten the index over the past six months as its stock price is up 26.6% thanks to its solid quarterly results.

Is there a buying opportunity in Tutor Perini, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Tutor Perini Not Exciting?

We’re happy investors have made money, but we're sitting this one out for now. Here are three reasons you should be careful with TPC and a stock we'd rather own.

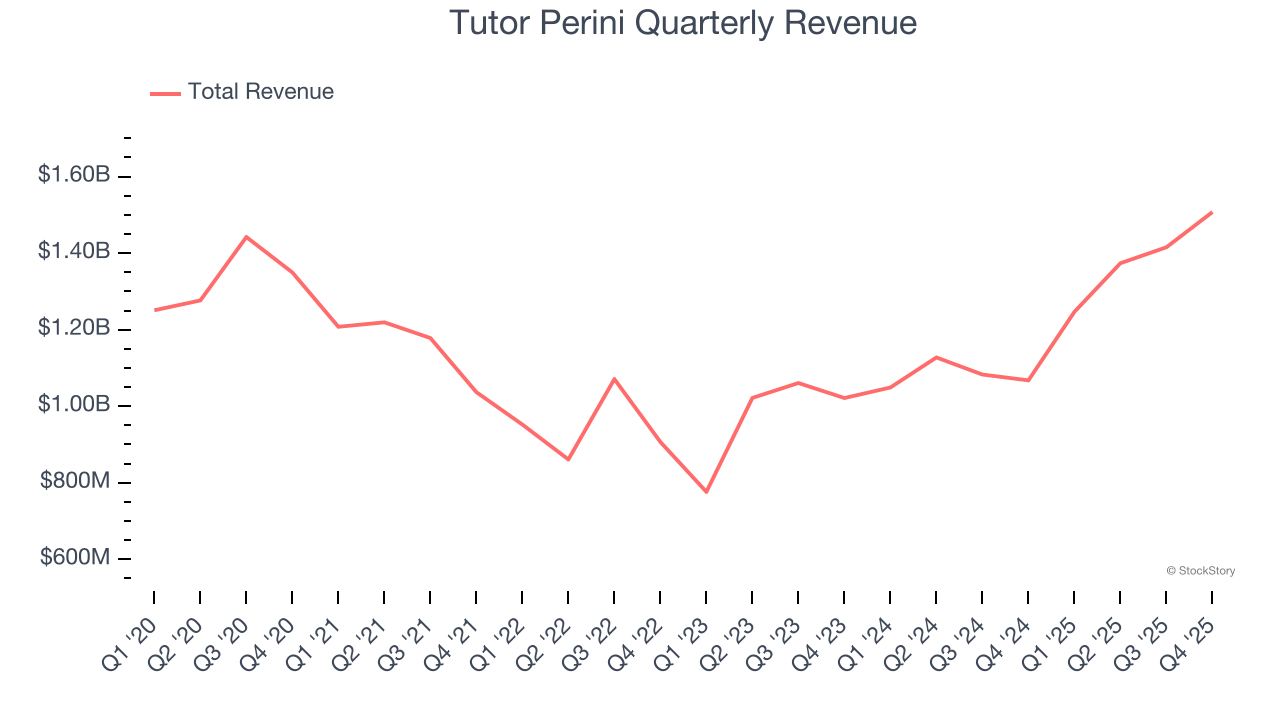

1. Long-Term Revenue Growth Flatter Than a Pancake

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Tutor Perini struggled to consistently increase demand as its $5.54 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and signals it’s a lower quality business.

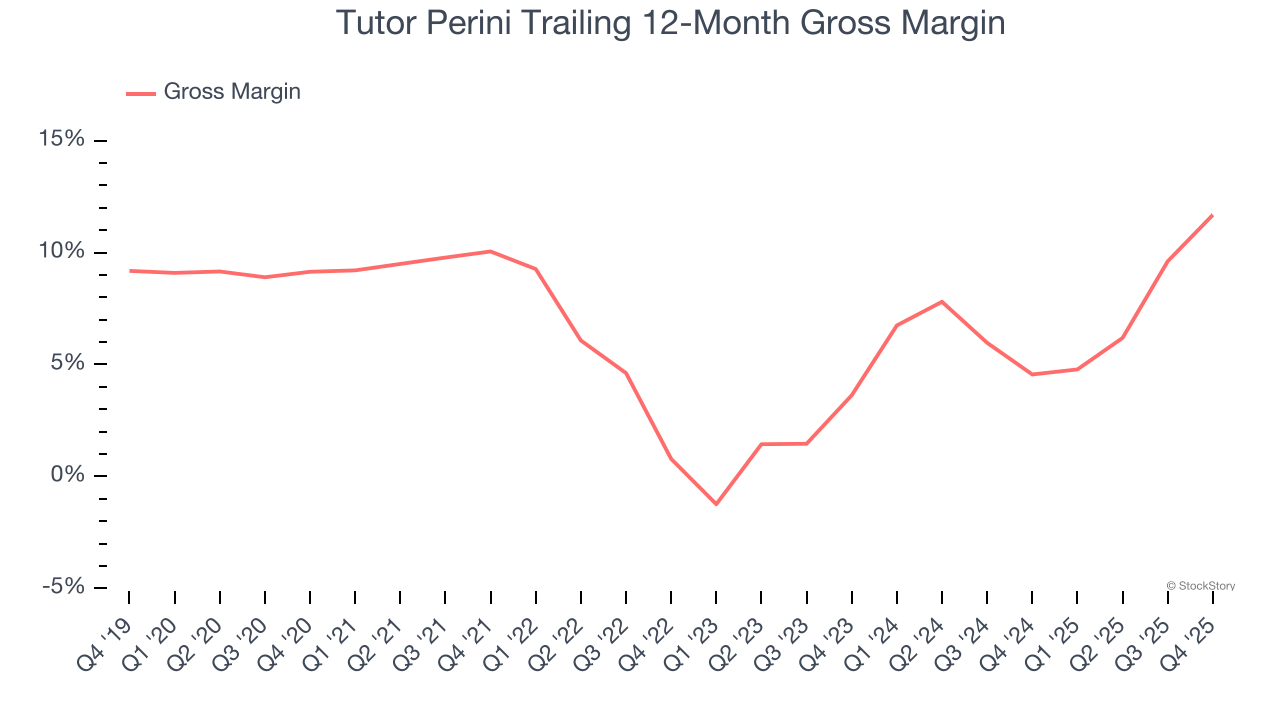

2. Low Gross Margin Reveals Weak Structural Profitability

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

Tutor Perini has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 6.7% gross margin over the last five years. That means Tutor Perini paid its suppliers a lot of money ($93.32 for every $100 in revenue) to run its business.

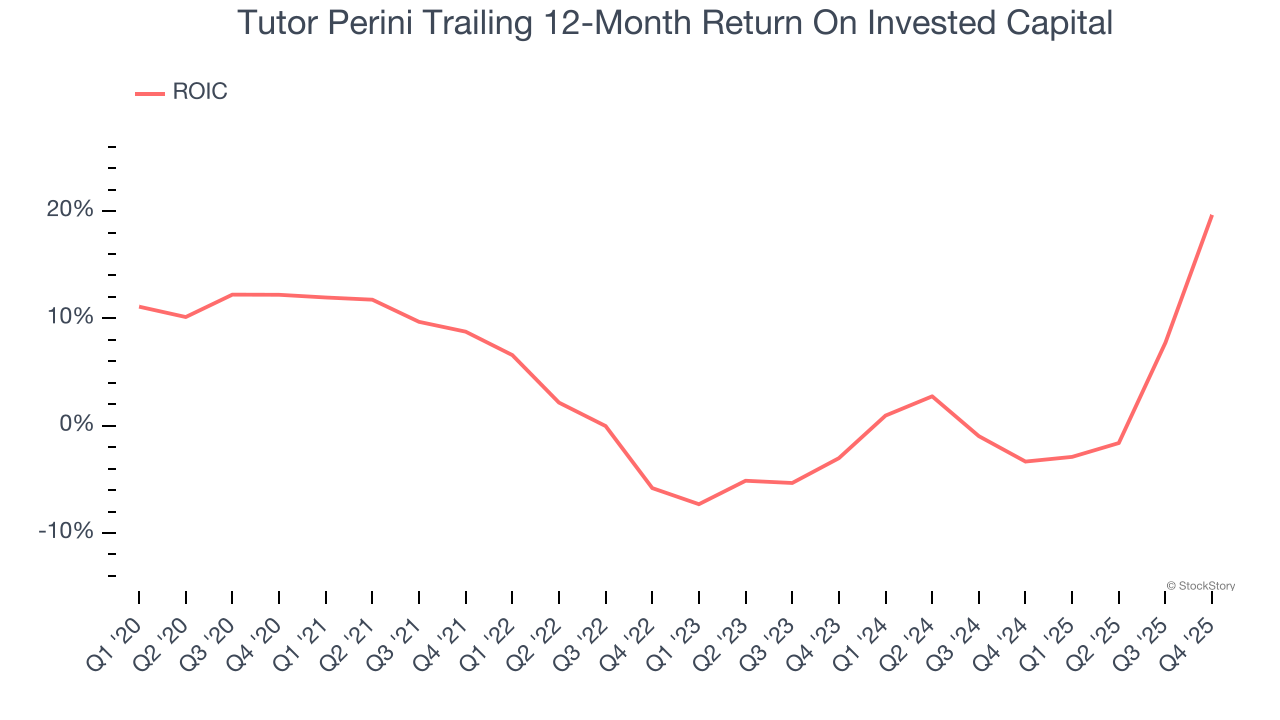

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Tutor Perini historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 3.2%, lower than the typical cost of capital (how much it costs to raise money) for industrials companies.

Final Judgment

Tutor Perini isn’t a terrible business, but it doesn’t pass our quality test. With its shares topping the market in recent months, the stock trades at 17× forward P/E (or $84.22 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward one of Charlie Munger’s all-time favorite businesses.

Stocks We Would Buy Instead of Tutor Perini

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.