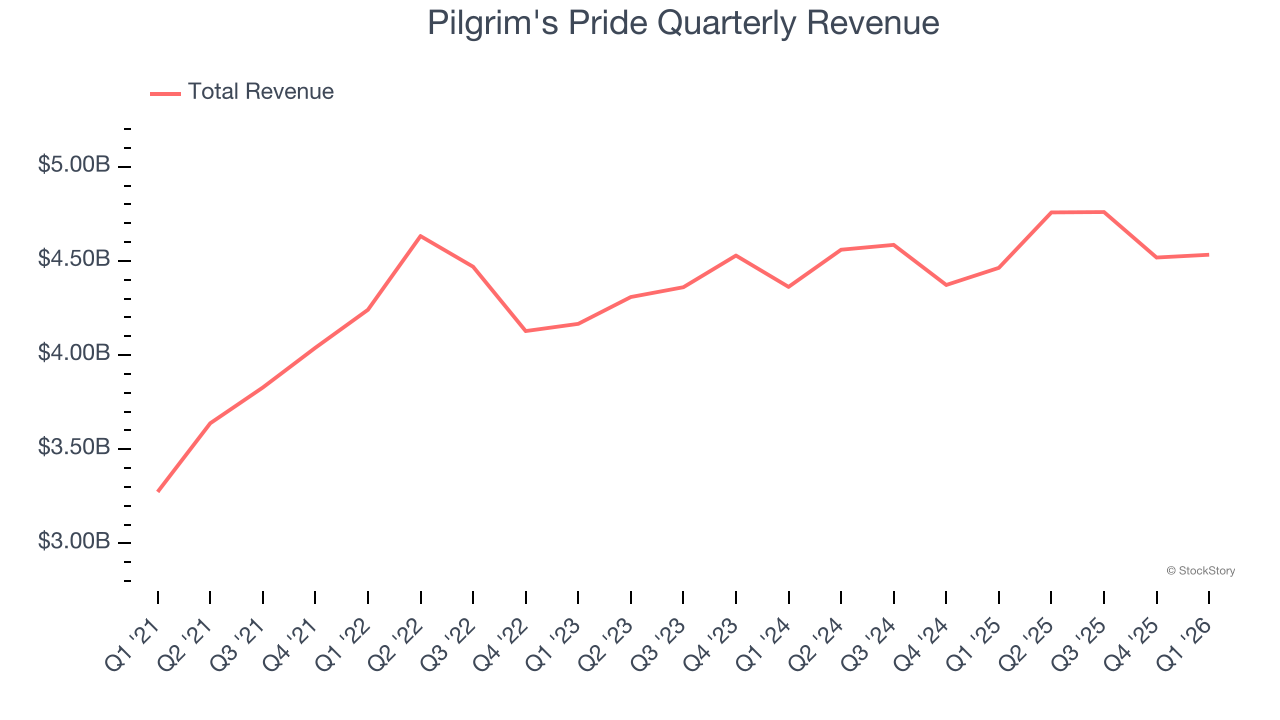

Chicken producer Pilgrim’s Pride (NASDAQ: PPC) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 1.6% year on year to $4.53 billion. Its non-GAAP profit of $0.51 per share was 21.2% below analysts’ consensus estimates.

Is now the time to buy Pilgrim's Pride? Find out by accessing our full research report, it’s free.

Pilgrim's Pride (PPC) Q1 CY2026 Highlights:

- Revenue: $4.53 billion vs analyst estimates of $4.42 billion (1.6% year-on-year growth, 2.6% beat)

- Adjusted EPS: $0.51 vs analyst expectations of $0.65 (21.2% miss)

- Adjusted EBITDA: $308.1 million vs analyst estimates of $367.4 million (6.8% margin, 16.1% miss)

- Operating Margin: 3.6%, down from 9.1% in the same quarter last year

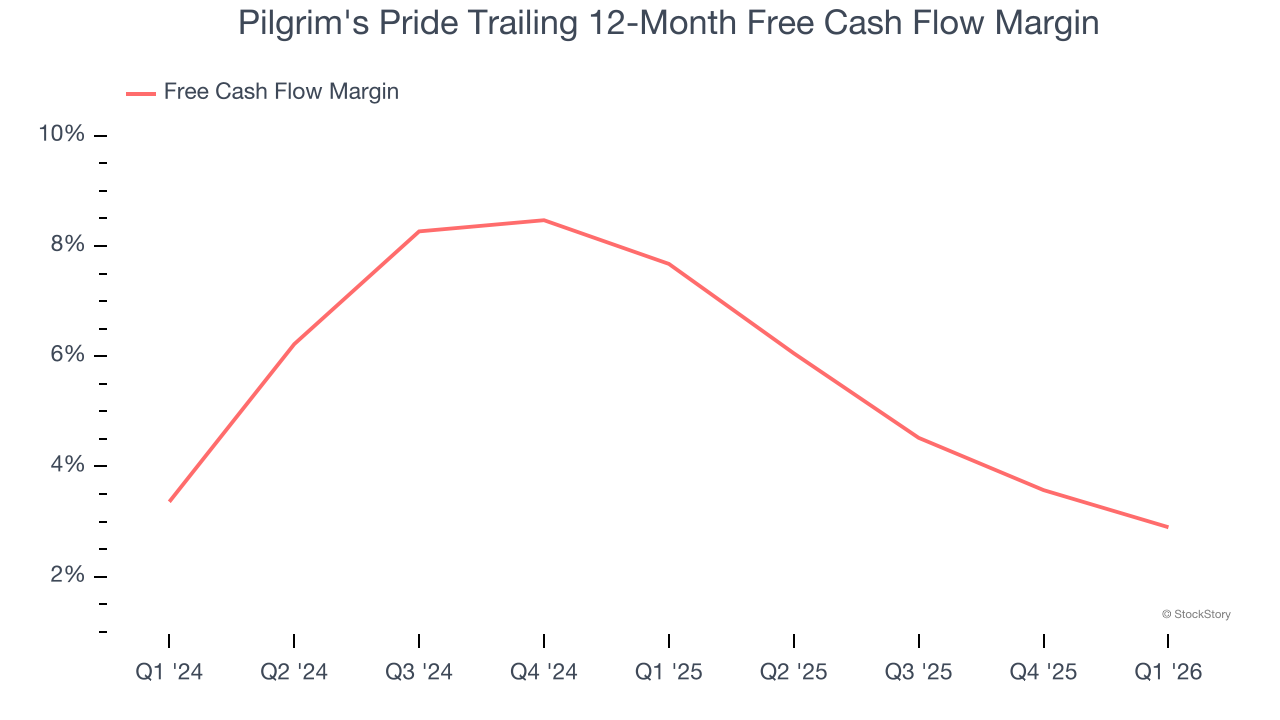

- Free Cash Flow was -$93.96 million, down from $28.62 million in the same quarter last year

- Market Capitalization: $7.82 billion

“During the quarter, chicken demand continued to be healthy across all regions,” said Fabio Sandri, Pilgrim’s President and CEO.

Company Overview

Offering everything from pre-marinated to frozen chicken, Pilgrim’s Pride (NASDAQ: PPC) produces, processes, and distributes chicken products to retailers and food service customers.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $18.57 billion in revenue over the past 12 months, Pilgrim's Pride is larger than most consumer staples companies and benefits from economies of scale, enabling it to gain more leverage on its fixed costs than smaller competitors. Its size also gives it negotiating leverage with distributors, allowing its products to reach more shelves. However, its scale is a double-edged sword because there are only a finite number of major retail partners, placing a ceiling on its growth. To accelerate sales, Pilgrim's Pride likely needs to optimize its pricing or lean into new products and international expansion.

As you can see below, Pilgrim's Pride’s 2.2% annualized revenue growth over the last three years was sluggish. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

This quarter, Pilgrim's Pride reported modest year-on-year revenue growth of 1.6% but beat Wall Street’s estimates by 2.6%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a slight deceleration versus the last three years. This projection doesn't excite us and implies its products will see some demand headwinds.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Pilgrim's Pride has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 5.2% over the last two years, slightly better than the broader consumer staples sector.

Taking a step back, we can see that Pilgrim's Pride’s margin dropped by 4.8 percentage points over the last year. If its declines continue, it could signal increasing investment needs and capital intensity.

Pilgrim's Pride burned through $93.96 million of cash in Q1, equivalent to a negative 2.1% margin. The company’s cash burn increased meaningfully year on year and is a deviation from its longer-term margin, indicating it is a seasonal business that must build up inventory during certain quarters.

Key Takeaways from Pilgrim's Pride’s Q1 Results

It was encouraging to see Pilgrim's Pride beat analysts’ revenue expectations this quarter. On the other hand, its adjusted operating income missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 1.4% to $30.71 immediately after reporting.

Pilgrim's Pride’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).