While the broader market has struggled with the S&P 500 down 2.1% since October 2025, Crown Holdings has surged ahead as its stock price has climbed by 6.6% to $102.76 per share. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Crown Holdings, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Crown Holdings Not Exciting?

We’re happy investors have made money, but we're sitting this one out for now. Here are three reasons why CCK doesn't excite us and a stock we'd rather own.

1. Long-Term Revenue Growth Disappoints

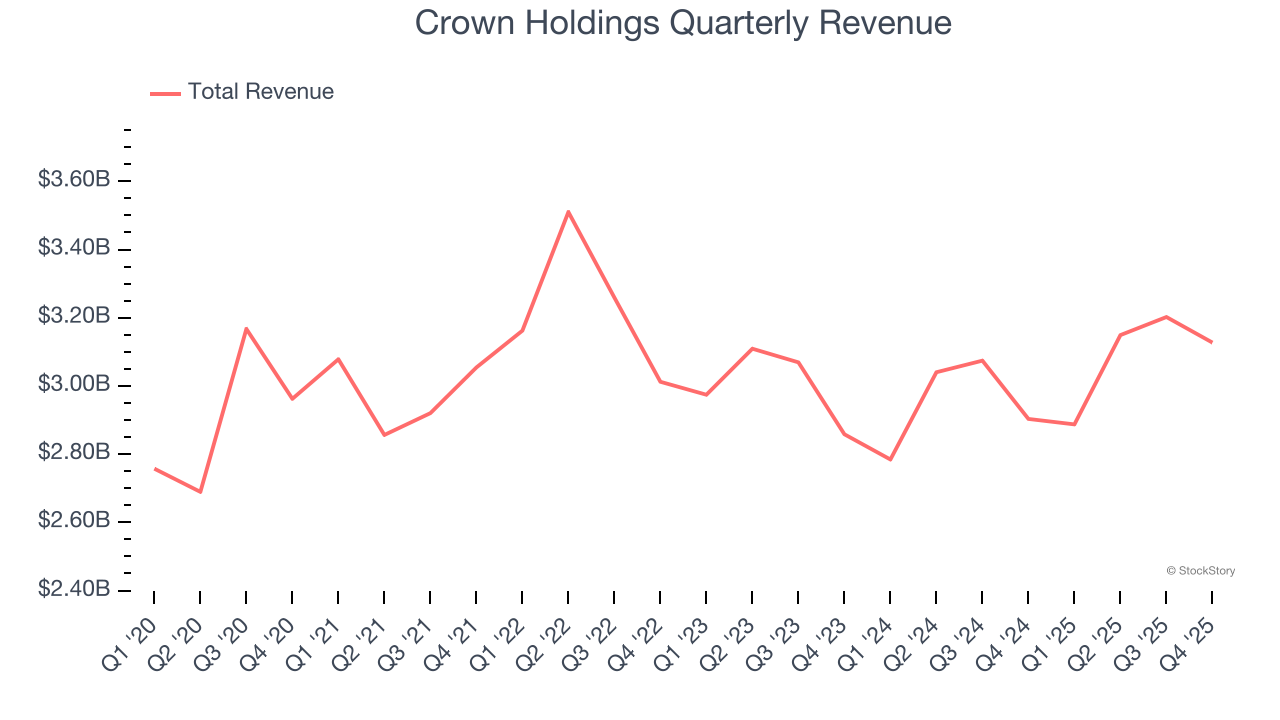

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Crown Holdings’s 1.3% annualized revenue growth over the last five years was weak. This fell short of our benchmarks.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Crown Holdings’s revenue to rise by 4%. Although this projection implies its newer products and services will catalyze better top-line performance, it is still below the sector average.

3. Low Gross Margin Reveals Weak Structural Profitability

Cost of sales for an industrials business is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics.

Crown Holdings has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 21.1% gross margin over the last five years. That means Crown Holdings paid its suppliers a lot of money ($78.85 for every $100 in revenue) to run its business.

Final Judgment

Crown Holdings isn’t a terrible business, but it doesn’t pass our bar. With its shares beating the market recently, the stock trades at 12.8× forward P/E (or $102.76 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at one of our all-time favorite software stocks.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.