Earnings results often indicate what direction a company will take in the months ahead. With Q1 behind us, let’s have a look at MACOM (NASDAQ: MTSI) and its peers.

Demand for analog chips is generally linked to the overall level of economic growth, as analog chips serve as the building blocks of most electronic goods and equipment. Unlike digital chip designers, analog chip makers tend to produce the majority of their own chips, as analog chip production does not require expensive leading edge nodes. Less dependent on major secular growth drivers, analog product cycles are much longer, often 5-7 years.

The 15 analog semiconductors stocks we track reported a strong Q1. As a group, revenues beat analysts’ consensus estimates by 1.5% while next quarter’s revenue guidance was 5.7% above.

Thankfully, share prices of the companies have been resilient as they are up 7.4% on average since the latest earnings results.

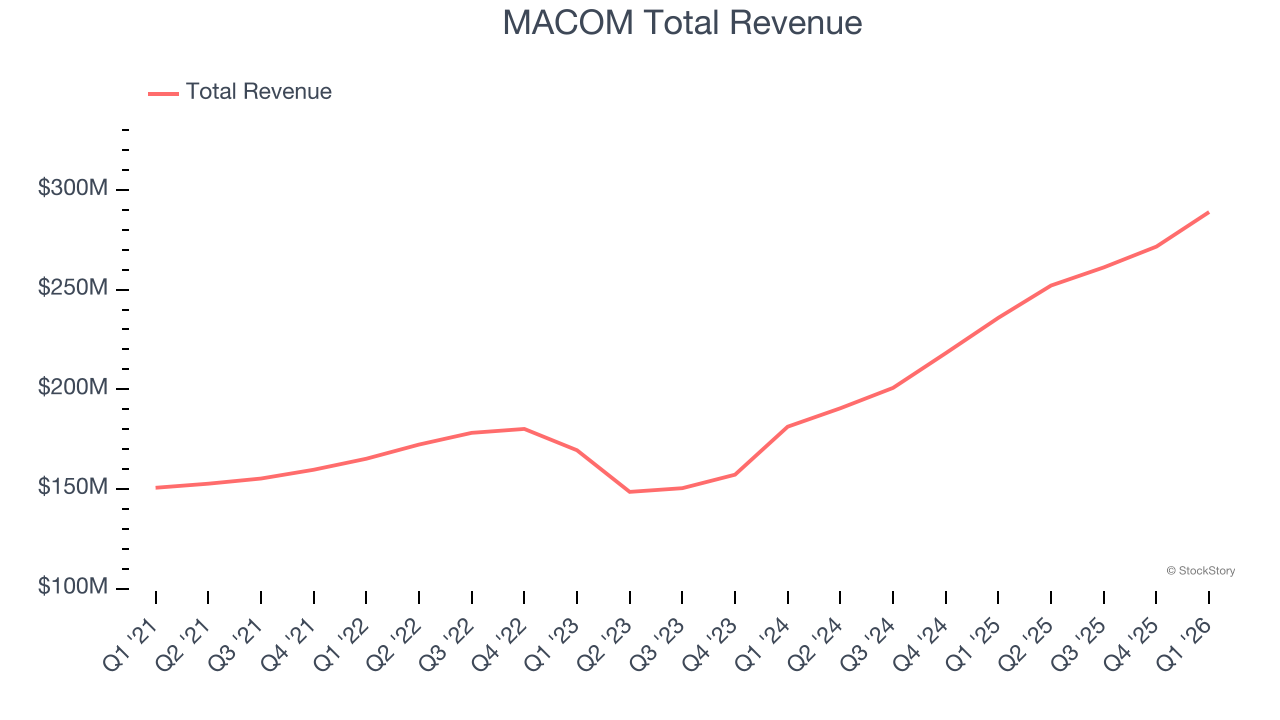

MACOM (NASDAQ: MTSI)

Founded in the 1950s as Microwave Associates, a communications supplier to the US Army Signal Corp, today MACOM Technology Solutions (NASDAQ: MTSI) is a provider of analog chips used in optical, wireless, and satellite networks.

MACOM reported revenues of $289 million, up 22.5% year on year. This print exceeded analysts’ expectations by 1.2%. Overall, it was a strong quarter for the company with revenue guidance for next quarter exceeding analysts’ expectations and a decent beat of analysts’ operating income estimates.

“We are pleased with our first half fiscal year results and look forward to strong revenue growth and profitability in the second half,” said Stephen G. Daly, President and Chief Executive Officer, MACOM.

MACOM scored the highest guidance raise of the whole group. Unsurprisingly, the stock is up 13.5% since reporting and currently trades at $351.50.

Is now the time to buy MACOM? Access our full analysis of the earnings results here, it’s free.

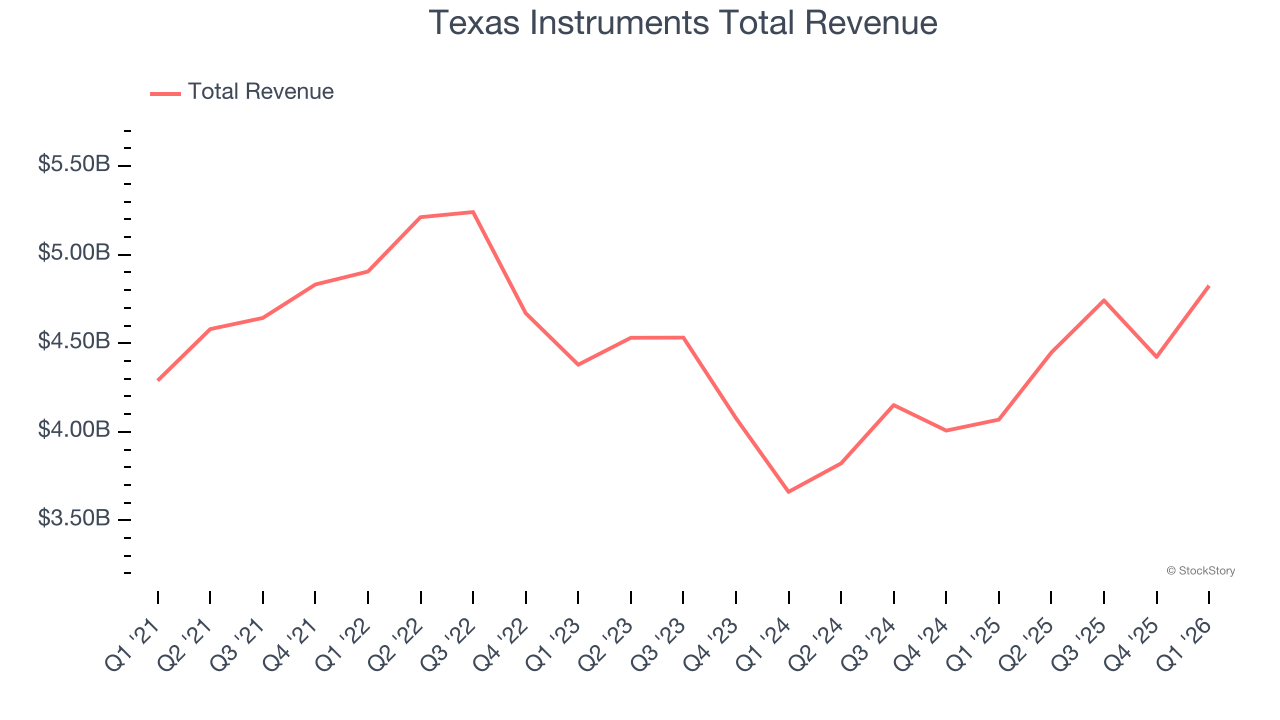

Best Q1: Texas Instruments (NASDAQ: TXN)

Headquartered in Dallas, Texas since the 1950s, Texas Instruments (NASDAQ: TXN) is the world’s largest producer of analog semiconductors.

Texas Instruments reported revenues of $4.83 billion, up 18.6% year on year, outperforming analysts’ expectations by 6.6%. The business had a stunning quarter with a beat of analysts’ EPS and operating income estimates.

Texas Instruments delivered the biggest analyst estimate beat among its peers. The market seems happy with the results as the stock is up 25.4% since reporting. It currently trades at $296.45.

Is now the time to buy Texas Instruments? Access our full analysis of the earnings results here, it’s free.

Slowest Q1: Universal Display (NASDAQ: OLED)

Serving major consumer electronics manufacturers, Universal Display (NASDAQ: OLED) is a provider of organic light emitting diode (OLED) technologies used in display and lighting applications.

Universal Display reported revenues of $142.2 million, down 14.5% year on year, falling short of analysts’ expectations by 11%. It was a disappointing quarter as it posted full-year revenue guidance missing analysts’ expectations.

Universal Display delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 4% since the results and currently trades at $83.63.

Read our full analysis of Universal Display’s results here.

Monolithic Power Systems (NASDAQ: MPWR)

Founded in 1997 by its longtime CEO Michael Hsing, Monolithic Power Systems (NASDAQ: MPWR) is an analog and mixed signal chipmaker that specializes in power management chips meant to minimize total energy consumption.

Monolithic Power Systems reported revenues of $804.2 million, up 26.1% year on year. This number topped analysts’ expectations by 2.8%. Overall, it was a very strong quarter as it also put up revenue guidance for next quarter exceeding analysts’ expectations and a solid beat of analysts’ operating income estimates.

The stock is down 16.9% since reporting and currently trades at $1,341.

Read our full, actionable report on Monolithic Power Systems here, it’s free.

Impinj (NASDAQ: PI)

Founded by Caltech professor Carver Mead and one of his students Chris Diorio, Impinj (NASDAQ: PI) is a maker of radio-frequency identification (RFID) hardware and software.

Impinj reported revenues of $74.25 million, flat year on year. This print surpassed analysts’ expectations by 2.4%. Zooming out, it was a satisfactory quarter as it also recorded an impressive beat of analysts’ operating income estimates but an increase in its inventory levels.

The stock is up 19.7% since reporting and currently trades at $143.74.

Read our full, actionable report on Impinj here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.