Shareholders of Upwork would probably like to forget the past six months even happened. The stock has dropped 38.7% and now trades at a new 52-week low of $10.35. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Given the weaker price action, is this a buying opportunity for UPWK? Find out in our full research report, it’s free.

Why Does UPWK Stock Spark Debate?

Formed through the 2013 merger of Elance and oDesk, Upwork (NASDAQ: UPWK) is an online platform where businesses and independent professionals connect to get work done.

Two Positive Attributes:

1. Eye-Popping Growth in Customer Spending

Average revenue per customer (ARPC) is a critical metric to track because it measures how much the company earns in transaction fees from each customer. This number also informs us about Upwork’s take rate, which represents its pricing leverage over the ecosystem, or "cut" from each transaction.

Upwork’s ARPC growth has been exceptional over the last two years, averaging 10.1%. Although its active clients shrank during this time, the company’s ability to successfully increase monetization demonstrates its platform’s value for existing customers.

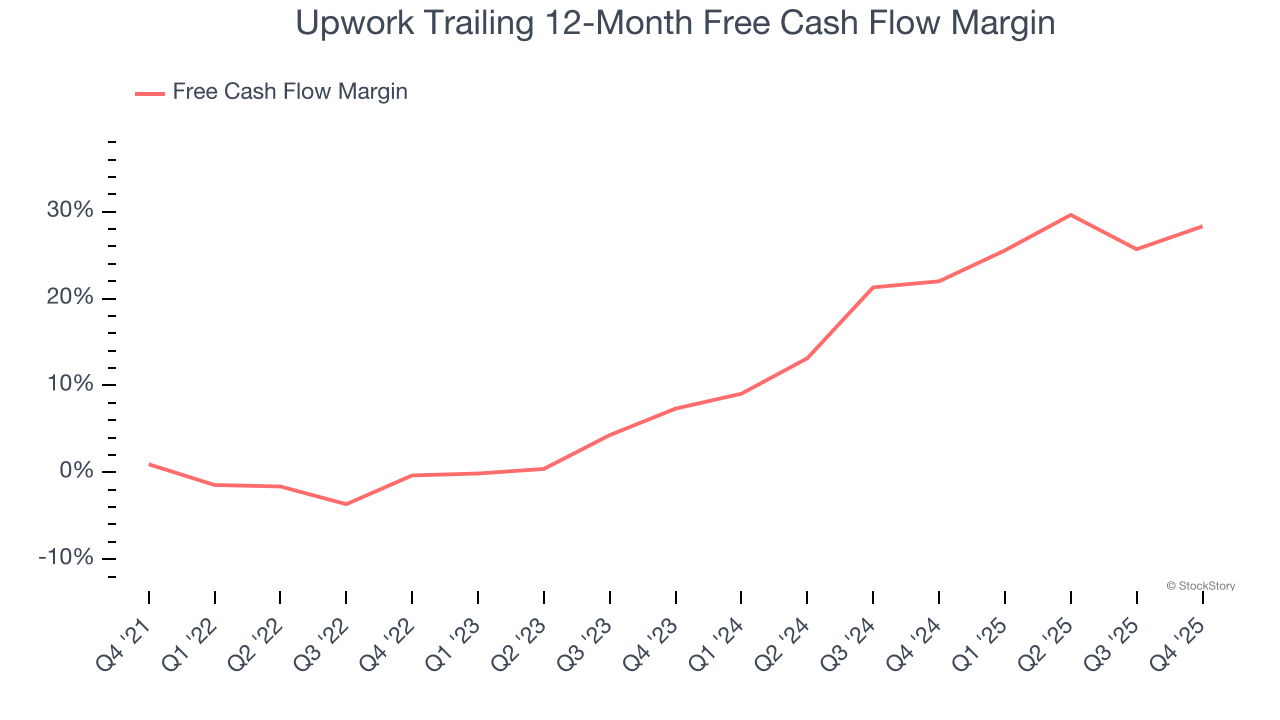

2. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Upwork has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the consumer internet sector, averaging 25.2% over the last two years.

One Reason to be Careful:

Declining Active Clients Reflect Product Weakness

As a gig economy marketplace, Upwork generates revenue growth by expanding the number of services on its platform (e.g. rides, deliveries, freelance jobs) and raising the commission fee from each service provided.

Upwork struggled with new customer acquisition over the last two years as its active clients have declined by 7% annually to 785,000 in the latest quarter. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Upwork wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

Final Judgment

Upwork’s merits more than compensate for its flaws. After the recent drawdown, the stock trades at 4.8× forward EV/EBITDA (or $10.35 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Upwork

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.