Since October 2025, Labcorp has been in a holding pattern, posting a small loss of 1.9% while floating around $272.50. The stock also fell short of the S&P 500’s 3.5% gain during that period.

Is there a buying opportunity in Labcorp, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Labcorp Not Exciting?

We're cautious about Labcorp. Here are three reasons we avoid LH and a stock we'd rather own.

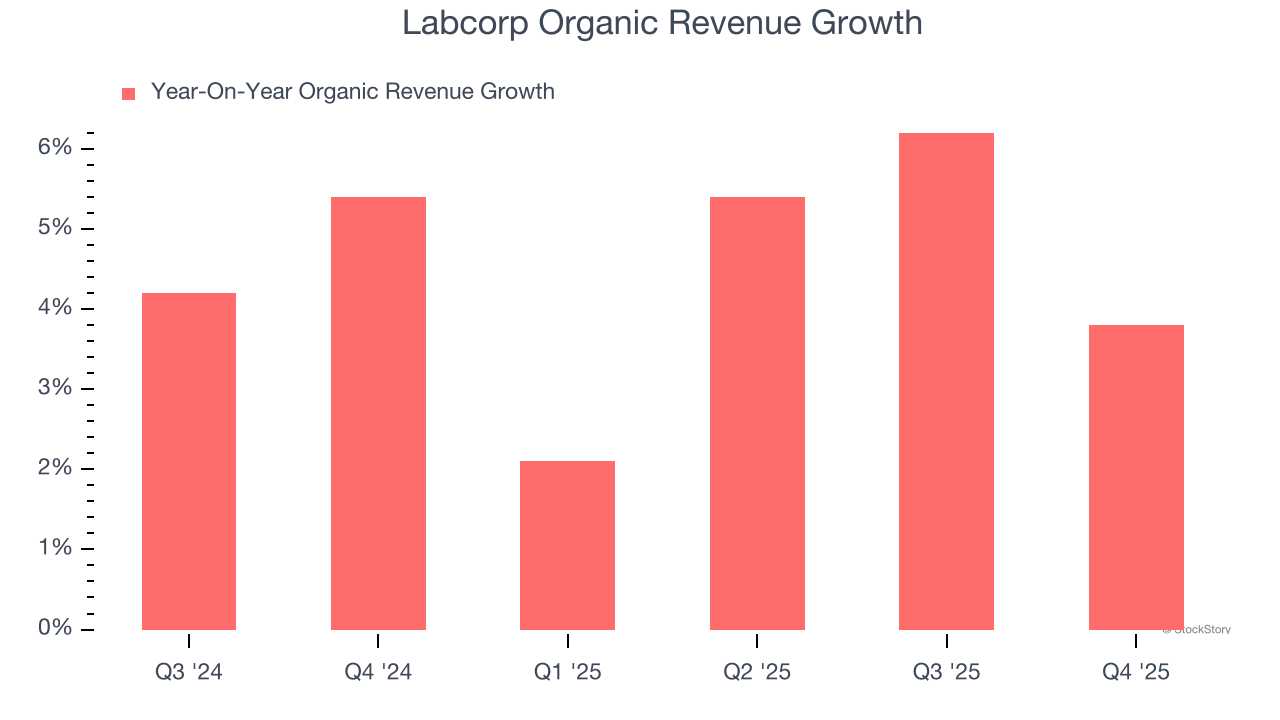

1. Slow Organic Growth Suggests Waning Demand In Core Business

Investors interested in Testing & Diagnostics Services companies should track organic revenue in addition to reported revenue. This metric gives visibility into Labcorp’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Labcorp’s organic revenue averaged 4.5% year-on-year growth. This performance slightly lagged the sector and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

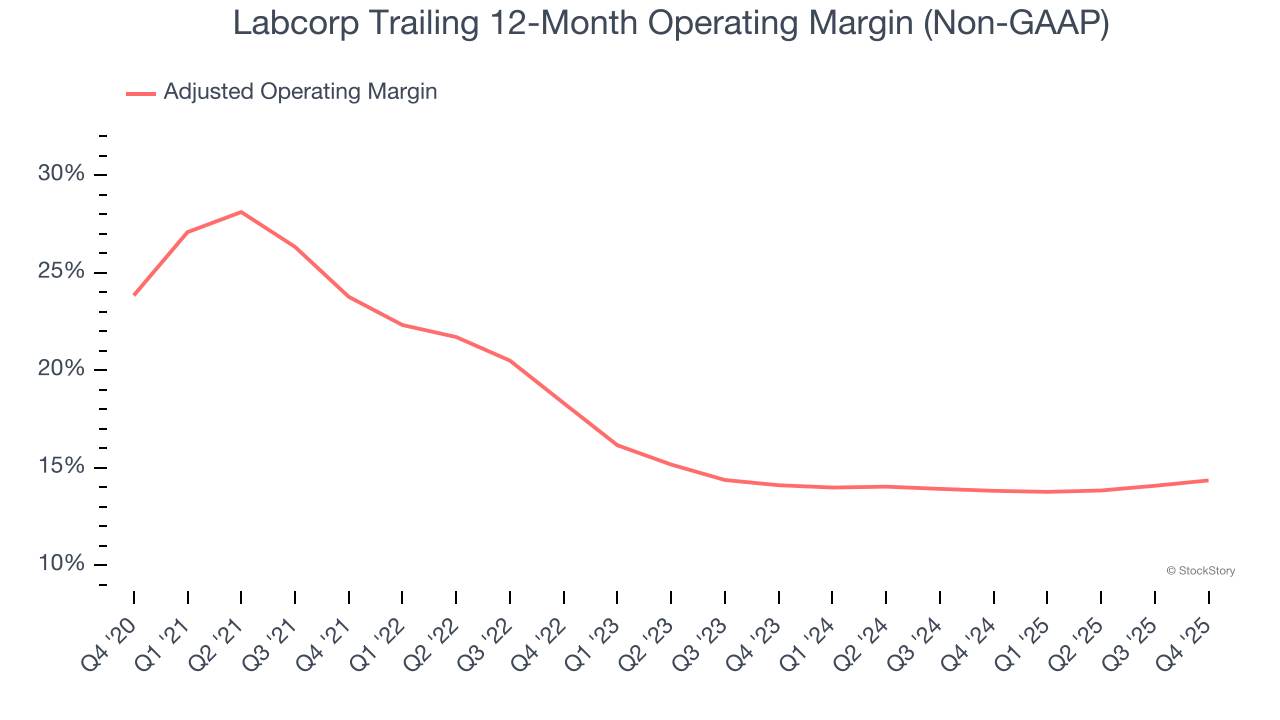

2. Shrinking Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

Looking at the trend in its profitability, Labcorp’s adjusted operating margin decreased by 9.4 percentage points over the last five years. Even though its historical margin was healthy, shareholders will want to see Labcorp become more profitable in the future. Its adjusted operating margin for the trailing 12 months was 14.3%.

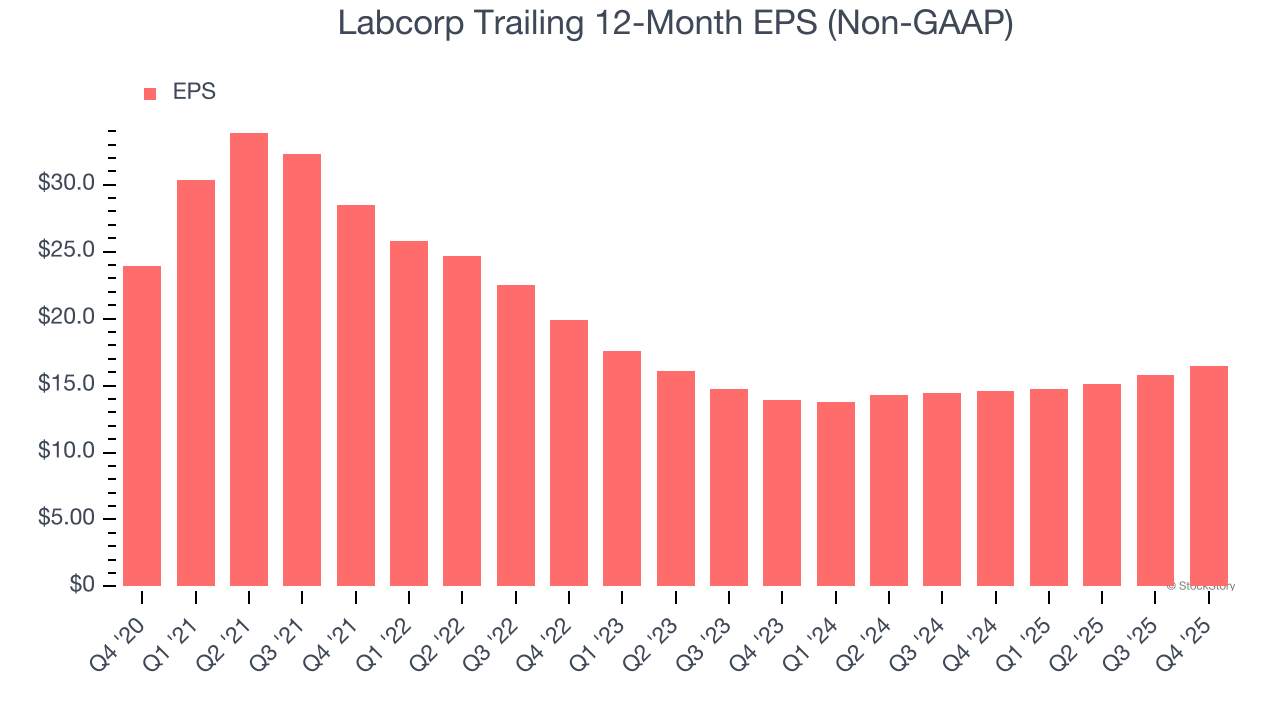

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Labcorp, its EPS declined by 7.2% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

Final Judgment

Labcorp isn’t a terrible business, but it doesn’t pass our quality test. With its shares underperforming the market lately, the stock trades at 15.4× forward P/E (or $272.50 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at the most entrenched endpoint security platform on the market.

Stocks We Like More Than Labcorp

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.