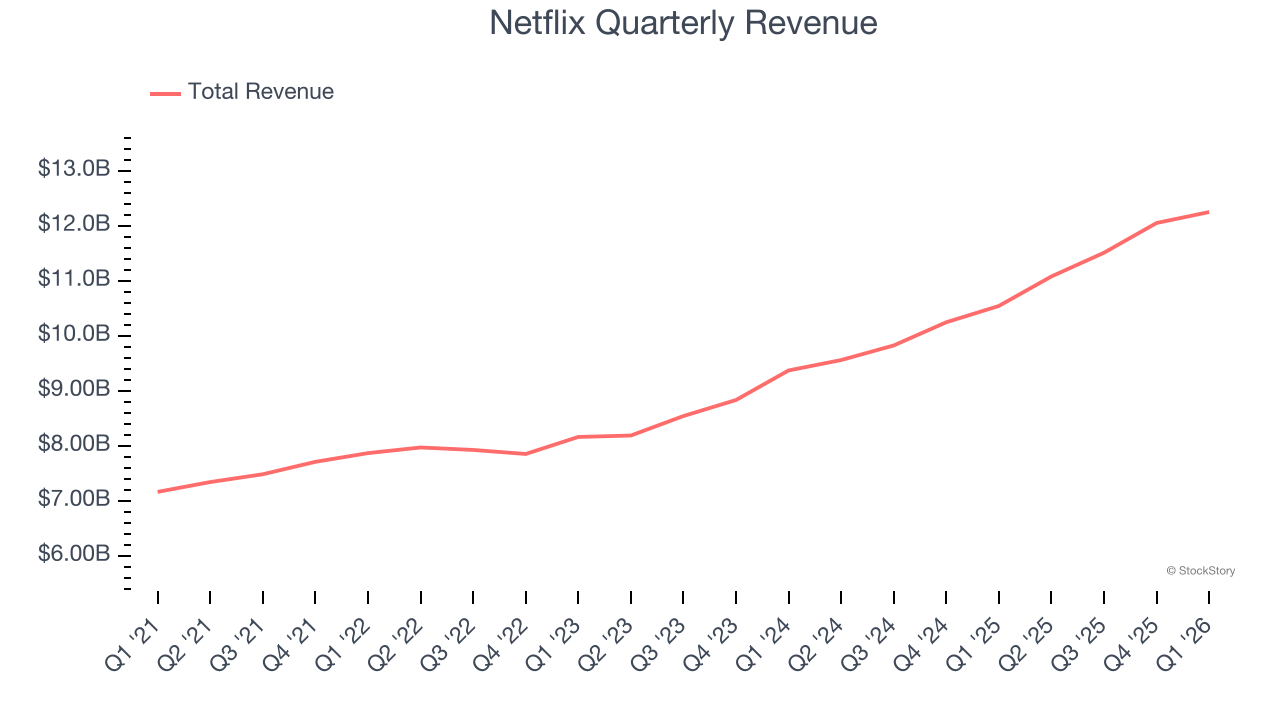

Streaming video giant Netflix (NASDAQ: NFLX) announced better-than-expected revenue in Q1 CY2026, with sales up 16.2% year on year to $12.25 billion. On the other hand, next quarter’s revenue guidance of $12.57 billion was less impressive, coming in 0.6% below analysts’ estimates. Its GAAP profit of $1.23 per share was 8.5% below analysts’ consensus estimates.

Is now the time to buy Netflix? Find out by accessing our full research report, it’s free.

Netflix (NFLX) Q1 CY2026 Highlights:

- Revenue: $12.25 billion vs analyst estimates of $12.19 billion (16.2% year-on-year growth, 0.5% beat)

- EPS (GAAP): $1.23 vs analyst expectations of $1.34 (8.5% miss)

- Adjusted Operating Income: $4.10 billion vs analyst estimates of $3.95 billion (33.4% margin, 3.7% beat)

- The company reconfirmed its revenue guidance for the full year of $51.2 billion at the midpoint

- EPS (GAAP) guidance for Q2 CY2026 is $0.78 at the midpoint, missing analyst estimates by 7.3%

- Operating Margin: 32.3%, in line with the same quarter last year

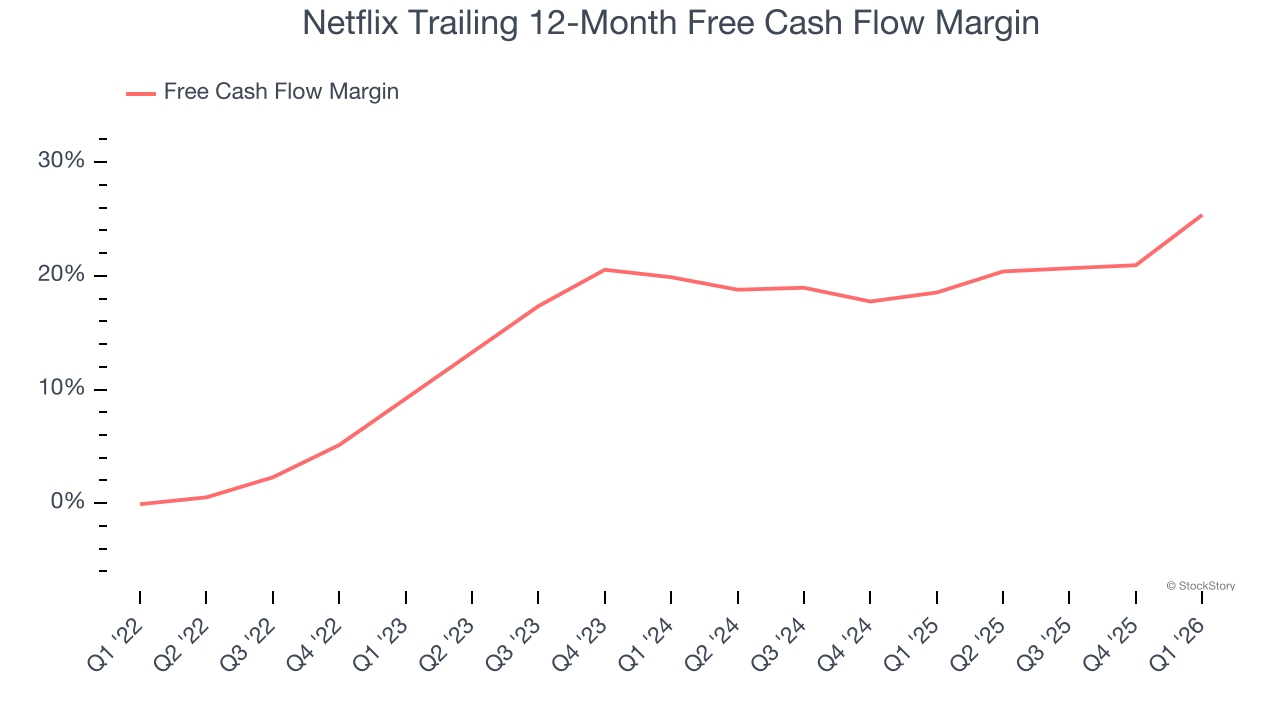

- Free Cash Flow Margin: 41.6%, up from 15.5% in the previous quarter

- Market Capitalization: $454.8 billion

Company Overview

Launched by Reed Hastings as a DVD mail rental company until its famous pivot to streaming in 2007, Netflix (NASDAQ: NFLX) is a pioneering streaming content platform.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last three years, Netflix grew its sales at a decent 13.7% compounded annual growth rate. Its growth was slightly above the average consumer internet company and shows its offerings resonate with customers.

This quarter, Netflix reported year-on-year revenue growth of 16.2%, and its $12.25 billion of revenue exceeded Wall Street’s estimates by 0.5%. Company management is currently guiding for a 13.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.3% over the next 12 months, similar to its three-year rate. This projection is particularly healthy for a company of its scale and indicates the market is forecasting success for its products and services.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Cash Is King

Although EBITDA is undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Netflix has shown terrific cash profitability, driven by its cost-effective customer acquisition strategy that enables it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the consumer internet sector, averaging 22.2% over the last two years.

Taking a step back, we can see that Netflix’s margin expanded by 16.2 percentage points over the last few years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Netflix’s free cash flow clocked in at $5.09 billion in Q1, equivalent to a 41.6% margin. This result was good as its margin was 16.3 percentage points higher than in the same quarter last year, building on its favorable historical trend.

Key Takeaways from Netflix’s Q1 Results

We struggled to find many positives in these results. Its EPS guidance for next quarter missed and its revenue guidance for next quarter fell slightly short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 5.9% to $97.86 immediately after reporting.

Netflix’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).